SUMMARY

Home Equity & HELOCs Explained: A Developer’s Guide to Leveraging Property in 2026

Unlock your home’s financial potential with this practical guide to home equity and HELOCs, tailored for developers in 2026.

Keywords: Home Equity, HELOC, Developer Finance

TABLE OF CONTENTS

1. Overview: Why Understanding Home Equity & HELOCs is Crucial for Developers in 2026

2. Demystifying Home Equity: Your Property’s Hidden Power

3. HELOCs vs. Home Equity Loans: Choosing Your Financial Tool

4. Strategic Applications for Developers in 2026

5. The Application Process & What to Expect

6. Important Considerations & Risks

7. Frequently Asked Questions

8. Wrap-Up: Making Smart Choices with Your Home Equity

1. Overview: Why Understanding Home Equity & HELOCs is Crucial for Developers in 2026

As a developer, you’re constantly seeking intelligent ways to fund projects, manage cash flow, and grow your wealth. While traditional financing routes are well-trodden, many overlook a powerful resource often lying dormant: the equity built up in their primary residence. In 2026, with an evolving economic landscape, understanding how to responsibly leverage your home equity through tools like Home Equity Lines of Credit (HELOCs) isn’t just smart personal finance; it’s a strategic business move.

Your home isn’t just a place to live; it’s a significant asset that can be converted into liquid capital. This capital can fuel your next property acquisition, cover unexpected project costs, or even provide a safety net for market fluctuations. This guide from Kwonglish will break down the intricacies of home equity and HELOCs, offering a practical roadmap for developers looking to maximize their financial potential this year.

KEY POINT

Home equity represents a significant, often untapped, source of capital for developers. Leveraging it wisely can unlock new opportunities for investment and business growth in 2026.

2. Demystifying Home Equity: Your Property’s Hidden Power

Before we dive into how to use it, let’s clarify what home equity actually is. Simply put, home equity is the portion of your home that you truly own. It’s calculated by subtracting your outstanding mortgage balance from your home’s current market value. For instance, if your home is appraised at $700,000 and you owe $300,000 on your mortgage, you have $400,000 in home equity.

Equity typically builds in three main ways:

1. Mortgage Payments: Each payment you make reduces your principal balance, directly increasing your equity. In the early years of a mortgage, a larger portion of your payment goes towards interest, but over time, more goes to principal.

2. Market Appreciation: When the value of your home increases due to market demand, local development, or inflation, your equity grows without you having to do anything. The housing market in 2026 continues to see regional variations, so understanding local trends is key.

3. Home Improvements: Strategic renovations and upgrades can significantly boost your home’s market value, thereby increasing your equity. Think kitchen remodels, bathroom renovations, or adding usable square footage. For developers, this is often a natural extension of their expertise.

KEY POINT

Your home equity is the difference between your home’s market value and your outstanding mortgage balance. It grows through principal payments, market appreciation, and value-adding home improvements.

Factors Affecting Equity Growth in 2026

The pace at which your equity accumulates can be influenced by several factors:

• Interest Rates: Higher mortgage interest rates mean a larger portion of your early payments go towards interest, slowing principal reduction. Conversely, lower rates accelerate equity build-up.

• Local Housing Market: A robust seller’s market with high demand and limited inventory will generally lead to faster appreciation. Researching local market forecasts for 2026 is crucial.

• Economic Stability: A strong economy with job growth and consumer confidence often supports a healthy real estate market, contributing to equity gains.

Understanding these dynamics allows you to better project your available equity and plan your financial strategies. Always get a professional appraisal to determine your current market value accurately when considering leveraging your equity.

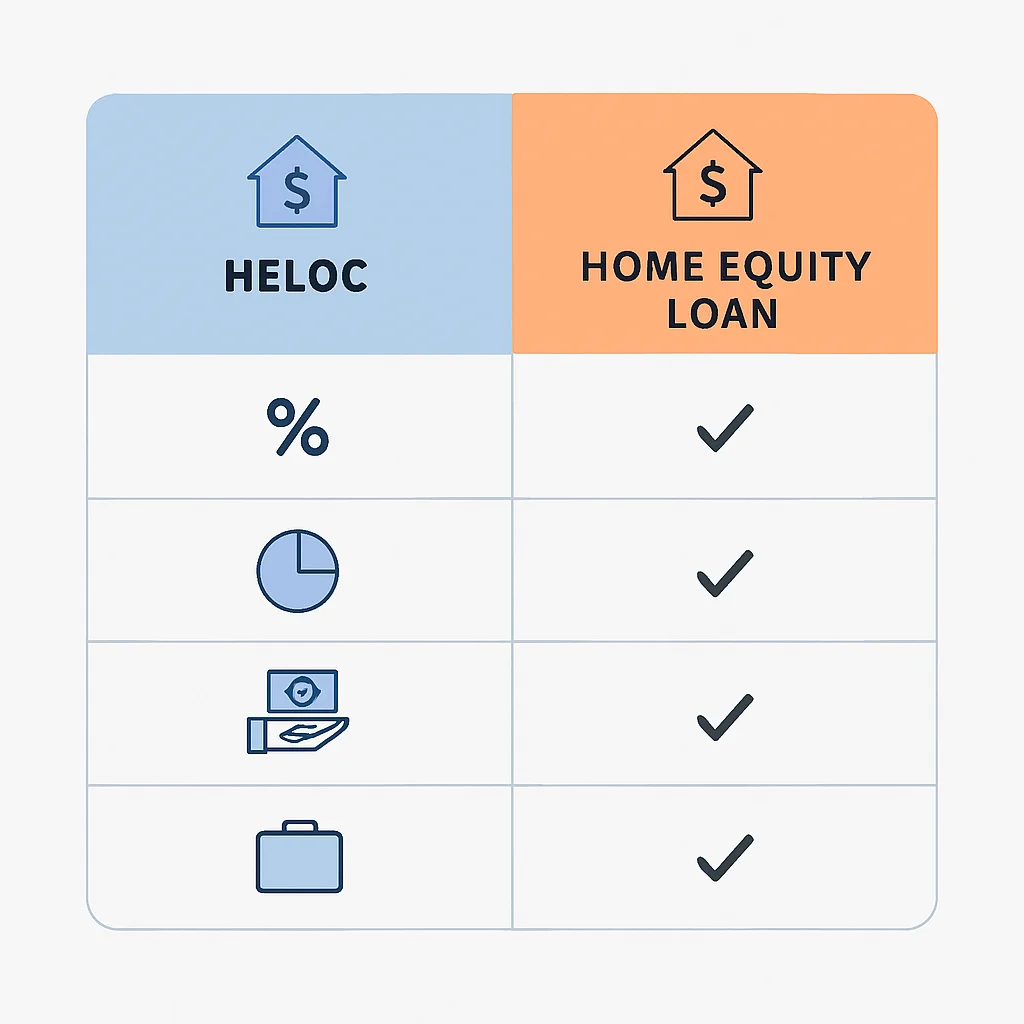

3. HELOCs vs. Home Equity Loans: Choosing Your Financial Tool

When it comes to tapping into your home equity, you primarily have two options: a Home Equity Loan (HEL) or a Home Equity Line of Credit (HELOC). While both use your home as collateral, they function very differently and are suited for different financial needs.

Home Equity Loan (HEL)

A Home Equity Loan is a second mortgage that provides you with a lump sum of cash upfront. You then repay this loan over a fixed period (e.g., 5, 10, 15 years) with fixed monthly payments and a fixed interest rate. This predictability makes it attractive for specific, one-time expenses.

Pros

✓ Fixed Interest Rate: Payments remain constant, making budgeting straightforward.

✓ Predictable Payments: Easy to plan for as they don’t change.

✓ Lump Sum: Ideal for large, one-time expenses like a significant renovation or a down payment on another property.

Cons

✗ Less Flexible: You receive all the money at once, whether you need it immediately or not.

✗ No Re-use: Once paid down, you cannot borrow against it again without applying for a new loan.

✗ Interest Paid on Full Amount: You start paying interest on the entire lump sum immediately, even if you don’t use it all at once.

Home Equity Line of Credit (HELOC)

A HELOC operates much like a credit card, but it’s secured by your home. You’re approved for a maximum borrowing limit, and you can draw funds as needed over a specific period, known as the “draw period” (typically 5-10 years). During the draw period, you usually only pay interest on the amount you’ve borrowed. Once the draw period ends, you enter the “repayment period” (typically 10-20 years), during which you repay both principal and interest.

Pros

✓ Flexibility: Borrow only what you need, when you need it, up to your credit limit.

✓ Revolving Credit: As you repay the principal, the funds become available to borrow again.

✓ Interest-Only Payments: Often available during the draw period, offering lower initial monthly obligations.

Cons

✗ Variable Interest Rate: Rates can fluctuate, leading to unpredictable monthly payments, especially in a changing interest rate environment like 2026.

✗ Balloon Payments: Payments can significantly increase when the draw period ends and principal repayment begins.

✗ Discipline Required: Easy access to funds can lead to overspending if not managed carefully.

KEY POINT

HELOCs offer flexibility with variable rates and revolving credit, ideal for ongoing needs. HELs provide predictability with fixed rates and lump sums, best for one-time, defined expenses. Choose based on your project’s funding structure and risk tolerance.

Interest Rate Considerations in 2026

As of 2026, the interest rate environment remains dynamic. While the Federal Reserve’s actions have stabilized somewhat, variable rates associated with HELOCs can still pose a risk. Typical HELOC rates are often tied to the prime rate plus a margin (e.g., Prime + 0.5% to 2%). If the prime rate increases, your HELOC payments will follow suit. For example, if the prime rate is 8.5% and your margin is 1%, your HELOC rate would be 9.5%. If the prime rate then jumps to 9%, your rate would become 10%.

Some lenders offer “hybrid” HELOCs that allow you to lock in a fixed rate on specific drawn amounts, providing a balance between flexibility and predictability. This could be a valuable option for developers planning projects with defined funding needs within a HELOC structure.

4. Strategic Applications for Developers in 2026

For developers, home equity and HELOCs are more than just emergency funds; they are powerful financial instruments that can be integrated into a broader investment strategy. Here are some strategic ways to use them in 2026:

Funding Investment Properties

One of the most common and effective uses for developers is to fund other real estate ventures. A HELOC can provide a flexible source of capital for:

• Down Payments: Instead of tying up liquid savings, use your HELOC for the 20-25% down payment on a new rental property or a fix-and-flip project. This allows you to acquire properties faster and potentially scale your portfolio.

• Renovation Costs: For fix-and-flip projects, a HELOC can cover material costs, contractor fees, and other renovation expenses. As you sell the renovated property, you can repay the HELOC, making the funds available again for your next project.

• Bridge Financing: Use a HELOC to bridge the gap between selling one property and acquiring another, ensuring you don’t miss out on time-sensitive opportunities.

Use Case: The Savvy Flipper

Kwonglish, a developer, has $200,000 in available HELOC funds. They identify a distressed property for $300,000 requiring $100,000 in renovations. Kwonglish uses $60,000 from their HELOC for the 20% down payment and another $100,000 for renovations. The property sells for $550,000 after 6 months. Kwonglish repays the $160,000 HELOC balance, plus interest, and still has substantial profit, while restoring their HELOC funds for the next flip.

Business Capital & Cash Flow Management

For developers running their own businesses, a HELOC can act as a flexible business line of credit. This can be particularly useful for:

• Working Capital: Covering operational expenses during lean periods, bridging gaps between project payments, or handling unexpected business costs.

• Equipment Purchases: Funding the acquisition of new machinery, tools, or software that can improve efficiency and capability.

• Expansion: Financing the opening of a new office, hiring additional staff, or investing in marketing efforts to grow your development business.

Use Case: Business Expansion

Kwonglish & Co. needs $75,000 to purchase specialized surveying equipment and hire two new project managers to take on larger contracts. Instead of seeking a traditional business loan with stricter terms, they use their HELOC. This provides immediate access to funds, allowing them to capitalize on a growing market demand in 2026 without disrupting their existing business credit lines.

Debt Consolidation

If you’re carrying high-interest debt, such as credit card balances (often 18-25% APR) or personal loans, a HELOC can offer a significantly lower interest rate. Consolidating these debts into a HELOC can simplify your payments and reduce your overall interest expense, freeing up cash flow for other investments. Be cautious, however, as you’re converting unsecured debt into secured debt against your home.

Use Case: Smart Debt Management

Kwonglish has $40,000 in credit card debt at an average interest rate of 20%. They secure a HELOC with an 8% variable interest rate. By drawing $40,000 from the HELOC to pay off the credit cards, Kwonglish reduces their annual interest payments from approximately $8,000 to $3,200 (assuming the HELOC rate remains stable). This saves them $4,800 annually, which can be reinvested or used for other financial goals.

Home Improvements

While not directly related to external development projects, using a HELOC for significant home improvements on your primary residence can increase its value and thus your equity. This can be a strategic move to prepare your home for future sale or simply enhance your living environment while potentially increasing your net worth.

KEY POINT

For developers, HELOCs are versatile tools for funding investment properties, providing business capital, consolidating high-interest debt, and making value-adding home improvements. Each use case requires careful financial planning and risk assessment.

5. The Application Process & What to Expect

Applying for a HELOC or Home Equity Loan involves a structured process that assesses your financial health and your home’s value. Here’s a breakdown of what to expect:

Eligibility Criteria

Lenders typically look for:

• Credit Score: A good to excellent credit score is usually required, often 680 or higher. A stronger score (e.g., 740+) can secure better interest rates.

• Loan-to-Value (LTV) Ratio: This is the amount of your mortgage divided by your home’s appraised value. Lenders typically allow you to borrow up to 80-85% of your home’s equity. For example, if your home is worth $700,000 and you owe $300,000, your equity is $400,000. An 80% LTV means you can borrow up to $560,000 ($700,000 x 0.80) in total debt (first mortgage + HELOC). Since your first mortgage is $300,000, you could potentially get a HELOC of up to $260,000 ($560,000 – $300,000).

• Debt-to-Income (DTI) Ratio: Your total monthly debt payments (including the proposed HELOC payment) should ideally be no more than 43% of your gross monthly income. Some lenders may go higher for strong applicants.

• Stable Income: Lenders want to see consistent income that demonstrates your ability to make repayments.

Required Documentation

Be prepared to provide:

• Proof of income (pay stubs, W-2s, tax returns for the last two years, especially if you’re self-employed).

• Bank statements.

• Mortgage statements for all existing loans on the property.

• Property tax statements and homeowner’s insurance policy.

• Identification (driver’s license, passport).

Step 1

Research & Compare Lenders

Look for banks, credit unions, and online lenders. Compare interest rates, fees, draw periods, repayment terms, and any special features like rate locks.

Step 2

Pre-qualification / Application

Submit an initial application, which may involve a soft credit pull. If pre-qualified, proceed with the full application and provide all necessary documentation.

Step 3

Home Appraisal

The lender will order a professional appraisal to determine your home’s current market value, which is critical for calculating your available equity.

Step 4

Underwriting & Approval

The lender’s underwriting team reviews all your documents and the appraisal to make a final decision. This typically takes 2-4 weeks after all documents are submitted.

Step 5

Closing & Funding

Attend closing to sign documents. For HELOCs, funds become available after a mandatory 3-day rescission period. For HELs, the lump sum is disbursed.

Typical Timeline & Costs

The entire process, from application to funding, can take anywhere from 2 to 6 weeks. Costs involved can include:

• Appraisal Fees: Typically $300-$500.

• Closing Costs: Can range from 2% to 5% of the credit line amount, covering title search, recording fees, and attorney fees. Some lenders offer no-closing-cost options, but these often come with slightly higher interest rates.

• Annual Fees: Some HELOCs charge an annual fee, typically $50-$100.

KEY POINT

A successful HELOC application hinges on a strong credit score, sufficient home equity (LTV typically < 85%), and a manageable DTI. Be prepared for a property appraisal and various closing costs, which can total 2-5% of the line amount.

6. Important Considerations & Risks

While leveraging your home equity offers significant advantages, it’s crucial to understand the inherent risks. As a developer, you’re accustomed to risk assessment, and your personal finances should be no different.

Variable Interest Rates

The most significant risk with a HELOC is its variable interest rate. If the prime rate (which HELOC rates are typically tied to) increases, your monthly payments will go up. This can strain your budget, especially if you’ve borrowed a large sum. For instance, if you have a $150,000 HELOC at Prime + 1% (e.g., 9.5% total) and the Prime Rate increases by 1%, your rate jumps to 10.5%. On an interest-only payment, this is an increase from $1,187.50 to $1,312.50 per month, a difference of $125. While seemingly small, these increases accumulate, and can be substantial when principal repayment begins.

Always factor in potential rate increases when calculating your affordability. Some HELOCs offer a “cap” on how high the interest rate can go, which provides some protection.

WARNING

Don’t Overleverage: Borrowing too much can lead to financial distress if interest rates rise or your income decreases. Always maintain a healthy buffer and an emergency fund.

Risk of Foreclosure

Because a HELOC or Home Equity Loan uses your home as collateral, failure to make payments can result in foreclosure. This is the most severe consequence and underscores the importance of responsible borrowing. Unlike unsecured debt, your home is directly at risk.

Impact on Credit Score

While opening a HELOC can initially cause a slight dip in your credit score due to a hard inquiry, responsible management can improve it over time. However, high utilization of your credit line (borrowing close to your limit) can negatively impact your credit score, as can missed payments. A high credit utilization ratio signals higher risk to lenders.

Market Downturns

If the housing market experiences a downturn, your home’s value could decrease. This could potentially leave you “underwater” on your loan, where you owe more than your home is worth. In extreme cases, lenders might even reduce your available credit line or freeze it, making it impossible to draw further funds when you might need them most.

KEY POINT

Always consult a qualified financial advisor before committing to a HELOC or Home Equity Loan. They can help you assess your personal financial situation, understand the terms, and navigate the risks in the context of your broader financial goals and the 2026 economic outlook.

Frequently Asked Questions

Q. What is the maximum LTV I can expect for a HELOC in 2026?

Most lenders in 2026 typically allow a combined loan-to-value (CLTV) ratio of 80-85%. This means your first mortgage balance plus the maximum HELOC amount generally cannot exceed 80-85% of your home’s appraised value.

Q. Are HELOC interest payments tax-deductible in 2026?

Under current tax law (as of 2026), interest on home equity loans and HELOCs is only deductible if the funds are used to buy, build, or substantially improve the home that secures the loan. It is not deductible if the funds are used for other purposes, such as debt consolidation or funding another investment property. Always consult a tax professional for personalized advice.

Q. How long is the typical draw period for a HELOC?

The draw period for a HELOC typically ranges from 5 to 10 years. During this time, you can borrow and repay funds as needed. After the draw period, the repayment period begins, usually lasting 10 to 20 years, during which you must repay both principal and interest on the outstanding balance.

Q. Can my HELOC be frozen or reduced by the lender?

Yes, lenders can freeze or reduce your available HELOC credit line under certain circumstances, such as a significant decline in your home’s value, a substantial change in your financial condition (e.g., job loss), or if you default on payments. This is a critical risk to be aware of.

7. Wrap-Up: Making Smart Choices with Your Home Equity

Your home equity is a powerful asset, and understanding how to unlock its potential through HELOCs or Home Equity Loans can be a game-changer for developers in 2026. Whether you’re funding a new investment property, injecting capital into your business, or strategically consolidating debt, these financial tools offer flexibility and access to capital that can accelerate your financial goals.

However, with great power comes great responsibility. The variable interest rates of HELOCs, the risk of foreclosure, and the potential impact of market fluctuations demand careful consideration and disciplined financial management. Always perform thorough due diligence, understand the terms of your loan, and, if in doubt, seek professional financial advice.

By approaching home equity with a strategic mindset and a clear understanding of both its benefits and risks, you can effectively leverage your primary residence to build a stronger financial future for yourself and your development ventures.

Thanks for reading, Kwonglish!

We hope this guide empowers you to make informed decisions about leveraging your home equity. Stay tuned for more practical financial insights from Kwonglish.

Got questions or a success story? Drop a comment below or share your thoughts on social media!