SUMMARY

Retirement Planning for Developers: Maximize Your 401(k) & Roth IRA in 2026

This guide provides practical advice for developers on how to optimize retirement savings through 401(k)s, Roth IRAs, and Solo 401(k)s to build long-term wealth.

Keywords: Retirement planning, 401k, Roth IRA, Solo 401k

TABLE OF CONTENTS

1. Overview: Why Retirement Planning is Critical for Developers

2. Maximizing Your 401(k) in 2026

3. Roth IRA Mastery: Tax-Free Growth and the Backdoor Strategy

4. Solo 401(k): A Powerhouse for Freelance Developers

5. Real-World Scenarios and Optimized Strategies

6. Important Caveats and Frequently Asked Questions (FAQ)

7. Wrap-Up: Secure Your Future, Starting Today

1. Overview: Why Retirement Planning is Critical for Developers

As a developer, you are likely in a high-income profession, which presents a unique opportunity to build substantial wealth for retirement. However, the fast-paced nature of the tech industry, along with potential burnout or a desire for early retirement, makes proactive financial planning essential. Many developers focus intensely on their craft, sometimes neglecting the crucial aspect of strategically saving and investing for the long term. This guide will walk you through the essential tax-advantaged retirement accounts available in 2026 – the 401(k), Roth IRA, and Solo 401(k) – and show you how to maximize them to secure your financial future.

The reality is, time is your most powerful asset when it comes to investing. Compound interest works wonders over decades. Starting early and consistently contributing to these accounts can turn seemingly small amounts into a formidable retirement nest egg. For instance, investing just $500 a month consistently from age 25 to 65 at an average annual return of 8% could accumulate over $1.7 million. Delaying that start by even 10 years significantly reduces the potential outcome, highlighting the urgency to act now, especially in 2026 with updated contribution limits and economic considerations.

Beyond just saving, understanding the nuances of these accounts – including their tax advantages, contribution rules, and withdrawal guidelines – is key to optimizing your wealth-building strategy. Developers often receive compensation in various forms, including base salary, bonuses, and Restricted Stock Units (RSUs) or stock options. Integrating these income streams into a robust retirement plan requires a clear understanding of how each account works and which one best suits your current financial situation and future goals.

KEY POINT

Starting early and consistently maximizing your tax-advantaged retirement accounts like the 401(k) and Roth IRA is the single most impactful action you can take to build substantial wealth for retirement. Even small, consistent contributions can grow exponentially over time due to compound interest.

2. Maximizing Your 401(k) in 2026

The 401(k) is often the cornerstone of many employees’ retirement plans, and for good reason. Offered by employers, it provides significant tax advantages and can be a powerful tool for wealth accumulation. Understanding its mechanics and how to leverage it effectively in 2026 is crucial.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows employees to contribute a portion of their pre-tax salary to investments, which then grow tax-deferred until retirement. Some plans also offer a Roth 401(k) option, which we will discuss shortly. The key benefit is that your contributions lower your taxable income in the current year, and you do not pay taxes on the investment gains until you withdraw the money in retirement.

Traditional vs. Roth 401(k) (2026 Contribution Limits)

Most 401(k) plans offer both a Traditional and a Roth option:

- Traditional 401(k): Contributions are made pre-tax, reducing your current taxable income. Your investments grow tax-deferred, and withdrawals in retirement are taxed as ordinary income. This is generally preferred if you expect to be in a lower tax bracket in retirement than you are now.

- Roth 401(k): Contributions are made with after-tax dollars. Your investments grow tax-free, and qualified withdrawals in retirement are completely tax-free. This is often advantageous if you expect to be in a higher tax bracket in retirement or want to diversify your tax exposure.

For 2026, the estimated maximum employee contribution limit for both Traditional and Roth 401(k)s is $23,500. If you are age 50 or older, you can make an additional catch-up contribution, estimated to be $7,500, bringing your total to $31,000. These figures are estimates based on historical inflation adjustments, as official IRS limits for 2026 are typically released in late 2025.

The Employer Match: Free Money You Can’t Afford to Miss

One of the most compelling reasons to contribute to your 401(k) is the employer match. Many companies will match a percentage of your contributions up to a certain limit. For example, an employer might match 50% of your contributions up to 6% of your salary. If you earn $150,000 and contribute 6% ($9,000), your employer would contribute an additional $4,500. This is essentially “free money” and represents an immediate, guaranteed return on your investment. Always contribute at least enough to get the full employer match.

KEY POINT

Always contribute at least enough to your 401(k) to receive the full employer match. Failing to do so is like turning down a guaranteed bonus, as it’s an immediate 50% or 100% return on your investment, depending on your company’s matching formula.

Investment Options within Your 401(k)

Your 401(k) plan typically offers a curated list of investment options, primarily mutual funds, Exchange Traded Funds (ETFs), and target-date funds. It is crucial to review these options regularly:

- Index Funds: These funds passively track a market index, like the S&P 500. They typically have very low expense ratios and offer broad market exposure.

- Target-Date Funds: These are “set-it-and-forget-it” funds that automatically adjust their asset allocation over time, becoming more conservative as you approach your target retirement year. They are a great option for those who prefer minimal involvement.

- Actively Managed Funds: These funds aim to outperform the market, but often come with higher expense ratios and may not consistently beat their benchmarks.

Pay close attention to expense ratios (fees). Even a difference of 0.5% in fees can cost you tens of thousands of dollars over decades. Opt for low-cost index funds or target-date funds whenever possible.

Advanced 401(k) Strategies for Developers

For high-income developers, there are advanced strategies to supercharge your 401(k) savings:

- Mega Backdoor Roth: If your employer’s 401(k) plan allows after-tax contributions and in-plan Roth conversions, you might be able to contribute significantly more than the standard $23,500 limit. The total 401(k) contribution limit (employee + employer + after-tax) for 2026 is estimated to be $70,000. This strategy involves contributing after-tax money to your 401(k) and then immediately converting it to a Roth account (either within the 401(k) or by rolling it into a Roth IRA). This effectively allows you to put a large sum into a Roth account, bypassing the Roth IRA income limits. Check with your plan administrator if this option is available.

- 401(k) Rollovers: When you leave an employer, you have a few options for your 401(k): leave it, cash it out (not recommended due to taxes and penalties), roll it into your new employer’s 401(k), or roll it into an IRA (Traditional or Roth, depending on the original account type and your tax strategy). Rolling into an IRA often provides more investment options and lower fees.

WARNING

Always consult a qualified financial advisor and tax professional before attempting complex strategies like the Mega Backdoor Roth. Incorrect execution can lead to significant tax penalties.

3. Roth IRA Mastery: Tax-Free Growth and the Backdoor Strategy

While your 401(k) is great, a Roth IRA offers unparalleled benefits, particularly tax-free growth and withdrawals in retirement. For many high-income developers, direct contributions to a Roth IRA are restricted, making the “backdoor Roth” strategy essential.

What is a Roth IRA?

A Roth IRA is an individual retirement account that allows your investments to grow tax-free, and qualified withdrawals in retirement are also tax-free. Contributions are made with after-tax dollars, meaning you do not get an upfront tax deduction. However, the long-term benefit of tax-free income in retirement is incredibly powerful.

2026 Contribution Limits & Income Phase-outs

For 2026, the estimated maximum contribution limit for a Roth IRA (and Traditional IRA) is $7,500. If you are age 50 or older, you can contribute an additional catch-up contribution, estimated to be $1,000, for a total of $8,500. These are estimates based on historical adjustments.

However, direct contributions to a Roth IRA are subject to income limitations. For 2026, if your Modified Adjusted Gross Income (MAGI) exceeds certain thresholds, your ability to contribute directly is phased out or eliminated. While official 2026 figures are pending, based on 2025 limits, it is safe to assume that most high-income developers (e.g., single filers earning over ~$160,000 or married filing jointly over ~$240,000) will likely be phased out of direct Roth IRA contributions. This is where the backdoor Roth strategy comes in.

The Backdoor Roth IRA Strategy: A Developer’s Best Friend

The backdoor Roth IRA allows high-income earners to indirectly contribute to a Roth IRA, bypassing the income limitations. It is a perfectly legal and widely used strategy. Here is how it works:

Step 1

Contribute to a Non-Deductible Traditional IRA

You contribute the maximum allowed amount (estimated $7,500 for 2026) to a Traditional IRA. Since your income is high, this contribution will be non-deductible, meaning you do not get a tax break for it this year. It is crucial that this Traditional IRA has a zero balance before you contribute, or that any existing Traditional IRA balances are rolled into a 401(k) to avoid the “pro-rata rule” (more on this below).

Step 2

Immediately Convert to a Roth IRA

After the contribution clears (usually a day or two), you immediately convert the entire balance of that Traditional IRA into a Roth IRA. Since the original contribution was non-deductible, this conversion is generally tax-free, except for any minimal earnings that might have accrued between contribution and conversion (which are usually negligible if done quickly).

Step 3

Report on Your Taxes (Form 8606)

You must file IRS Form 8606, “Nondeductible IRAs,” with your tax return. This form tracks your non-deductible contributions and ensures that the conversion is treated as tax-free. Your brokerage will also send you Form 1099-R for the distribution (conversion) and Form 5498 for the contribution.

KEY POINT

The “pro-rata rule” is a critical consideration for the backdoor Roth. If you have any pre-tax money in any Traditional, SEP, or SIMPLE IRAs (not 401(k)s), a portion of your Roth conversion will be taxable. To avoid this, roll any existing pre-tax IRA balances into your current 401(k) if your plan allows, before executing the backdoor Roth.

Example: Backdoor Roth IRA Steps in 2026

CODE EXPLANATION

This pseudo-code illustrates the logical steps and financial transactions involved in performing a Backdoor Roth IRA contribution for the 2026 tax year. It outlines the sequence of actions a developer would take with their brokerage account.

// Assume current date is early 2026

// Step 1: Ensure no pre-tax IRA balances (pro-rata rule check)

IF (CHECK_EXISTING_PRE_TAX_IRA_BALANCE() > 0) {

ROLLOVER_PRE_TAX_IRA_TO_401K(); // If employer 401(k) allows

// OR: Consult tax advisor for alternative strategies

}

// Step 2: Contribute to a Traditional IRA

DECLARE contributionAmount = 7500; // Estimated 2026 IRA contribution limit

CREATE_NEW_TRADITIONAL_IRA_ACCOUNT_IF_NOT_EXISTS();

CONTRIBUTE_FUNDS_TO_TRADITIONAL_IRA(contributionAmount, "NonDeductible");

WAIT_FOR_FUNDS_TO_SETTLE(); // Typically 1-2 business days

// Step 3: Convert Traditional IRA to Roth IRA

GET_TRADITIONAL_IRA_BALANCE(); // Should be ~contributionAmount + minimal earnings

INITIATE_ROTH_CONVERSION_FROM_TRADITIONAL_IRA(GET_TRADITIONAL_IRA_BALANCE());

WAIT_FOR_CONVERSION_TO_COMPLETE();

// Step 4: Invest funds within the Roth IRA

SELECT_INVESTMENTS_IN_ROTH_IRA(); // e.g., VOO, SPY, QQQ

// Step 5: Tax Reporting (Crucial!)

NOTE: Keep records of all transactions.

FILE_IRS_FORM_8606_WITH_2026_TAX_RETURN(); // Reports non-deductible contribution and conversion

EXPECT_FORM_1099R_FROM_BROKERAGE(); // For the conversion/distribution

EXPECT_FORM_5498_FROM_BROKERAGE(); // For the contribution

This process is typically done once a year. Many developers do it in January for the previous tax year, or anytime during the current tax year up until the tax filing deadline (usually April 15th of the following year, not including extensions). The key is to perform the contribution and conversion as close together as possible to minimize any taxable earnings.

4. Solo 401(k): A Powerhouse for Freelance Developers

For developers who freelance, consult, or have any self-employment income (even a side gig), the Solo 401(k) is an incredible retirement vehicle that offers significantly higher contribution limits than a traditional IRA or even a regular 401(k) in some cases.

Who is Eligible for a Solo 401(k)?

A Solo 401(k) (also known as an Individual 401(k) or Uni-401(k)) is designed for self-employed individuals with no full-time employees other than themselves or their spouse. If you are a freelance developer, a contractor, or run your own small tech business, and you do not employ anyone else full-time, you are likely eligible. You can even have a Solo 401(k) in addition to a regular 401(k) from an employer, as long as your self-employment income is separate.

2026 Contribution Limits: Maximize Your Savings

The power of the Solo 401(k) comes from its dual contribution structure: you can contribute as both an employee and an employer.

- As an Employee: You can contribute up to the standard 401(k) employee limit, estimated to be $23,500 for 2026. If you are age 50 or older, you can add an additional catch-up contribution of $7,500.

- As an Employer: Your business can contribute up to 25% of your net self-employment earnings (for a sole proprietor or single-member LLC) or 25% of your compensation (for an S-Corp).

The combined total of employee and employer contributions cannot exceed an estimated $70,000 for 2026 ($77,500 if age 50 or older). This is an incredibly high limit, allowing self-employed developers to shelter a significant portion of their income from taxes while saving for retirement.

Let us consider an example for 2026:

A freelance developer (sole proprietor) nets $100,000 from their self-employment business. They can contribute:

- Employee Contribution: $23,500

- Employer Contribution: 25% of their net self-employment earnings. For a sole proprietor, “net self-employment earnings” is calculated after deducting half of self-employment taxes and the employee 401(k) contribution. A simpler estimate is roughly 20% of gross self-employment income. So, approximately $20,000.

- Total: $23,500 (employee) + ~$20,000 (employer) = ~$43,500. This is well within the $70,000 overall limit.

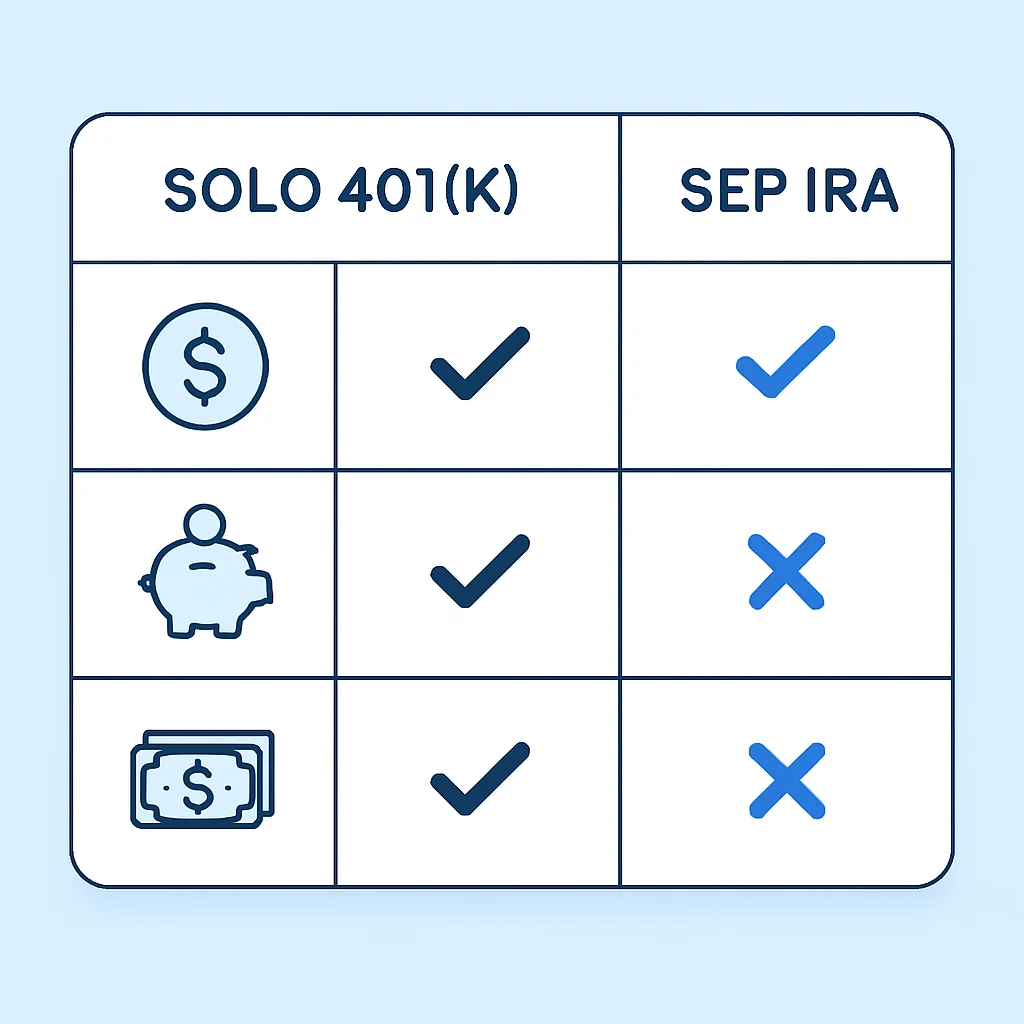

Solo 401(k) vs. SEP IRA

Another popular retirement account for the self-employed is the SEP IRA. While SEP IRAs also offer high contribution limits (up to 25% of net self-employment earnings, capped at $70,000 for 2026), the Solo 401(k) often comes out ahead for a few reasons:

- Higher Employee Contributions: With a Solo 401(k), you can always contribute the maximum employee deferral ($23,500 for 2026) regardless of your business’s profitability, as long as you have enough earned income. A SEP IRA only allows employer contributions, tied to a percentage of profit.

- Roth Option: Many Solo 401(k) providers offer a Roth option for the employee contribution portion, providing the benefit of tax-free withdrawals in retirement. SEP IRAs are always pre-tax.

- Loan Provision: Some Solo 401(k) plans allow you to borrow from your account, which is not possible with a SEP IRA.

- Mega Backdoor Roth Potential: Similar to an employer 401(k), some Solo 401(k) plans allow after-tax contributions, which can then be converted to a Roth Solo 401(k) or Roth IRA, leveraging the full $70,000 limit into a Roth structure.

KEY POINT

For self-employed developers, the Solo 401(k) often provides more flexibility and higher Roth contribution potential compared to a SEP IRA, making it a superior choice for maximizing tax-advantaged savings.

5. Real-World Scenarios and Optimized Strategies

Let us apply these concepts to common developer scenarios to illustrate how you can optimize your retirement savings in 2026.

Scenario 1: New Grad Developer (Age 22-25, First Job)

Case: Junior Dev, $90,000 Salary, 4% Employer 401(k) Match

Focus on establishing good habits and leveraging employer benefits early.

✓ Step 1: Maximize Employer 401(k) Match. Contribute at least 4% ($3,600) to get the full employer match ($3,600). This is a 100% immediate return.

✓ Step 2: Max Out Roth IRA. Contribute the full estimated $7,500 to a Roth IRA. As a new grad, you are likely below the income phase-out limits for direct contributions, and the tax-free growth is invaluable over a long career.

✓ Step 3: Increase 401(k) Contributions. After maxing the Roth IRA, increase your 401(k) contributions towards the estimated $23,500 limit. If you have a Roth 401(k) option, consider contributing here for more tax diversification.

✓ Step 4: Consider an HSA. If you have a High-Deductible Health Plan (HDHP), contribute to an HSA for its triple tax advantage (tax-deductible contributions, tax-free growth, tax-free withdrawals for medical expenses).

Scenario 2: Mid-Career Developer (Age 30-45, $180,000 Salary, Family)

Case: Senior Dev, $180,000 Salary, Married, 6% Employer 401(k) Match, High Income

Focus on maximizing all available tax-advantaged space, including backdoor strategies.

✓ Step 1: Maximize Employer 401(k) Match. Contribute at least 6% ($10,800) to get the full employer match ($10,800). This is non-negotiable.

✓ Step 2: Max Out Backdoor Roth IRA. Since your income likely exceeds the direct contribution limits, execute the backdoor Roth strategy for yourself and your spouse (if applicable), contributing an estimated $7,500 each for a total of $15,000 to Roth IRAs.

✓ Step 3: Max Out 401(k). Contribute the full estimated $23,500 to your 401(k). Consider a Roth 401(k) if available for tax diversification, especially if you expect to be in a higher tax bracket in retirement.

✓ Step 4: Max Out HSA. If you have an HDHP, contribute the full family limit (estimated $8,550 for 2026) to an HSA. Treat it as an additional retirement account if you do not need the funds for current medical expenses.

✓ Step 5: Mega Backdoor Roth. If your 401(k) plan allows after-tax contributions, explore the Mega Backdoor Roth to convert additional funds into a Roth account, up to the overall estimated $70,000 401(k) limit.

✓ Step 6: Taxable Brokerage Account. After exhausting all tax-advantaged accounts, invest in a taxable brokerage account for additional wealth building.

Scenario 3: Senior Developer (Age 50+, Considering Early Retirement)

Case: Principal Engineer, $250,000 Salary, Self-Employed Side Business, Age 52

Leverage catch-up contributions and self-employment accounts to accelerate savings for early retirement.

✓ Step 1: Max Out Employer 401(k) (including catch-up). Contribute the full estimated $23,500 + $7,500 catch-up = $31,000 to your employer 401(k). Don’t forget the employer match!

✓ Step 2: Max Out Backdoor Roth IRA (including catch-up). Execute the backdoor Roth for the full estimated $7,500 + $1,000 catch-up = $8,500.

✓ Step 3: Max Out Solo 401(k). With a side business, you can contribute as both employee and employer to a Solo 401(k). Maximize the employee portion ($23,500 + $7,500 catch-up = $31,000) and then the employer portion (up to 25% of net self-employment earnings), up to the overall estimated $77,500 limit. This can significantly boost your retirement savings.

✓ Step 4: Max Out HSA (including catch-up). If eligible, contribute the full family limit plus the $1,000 catch-up (estimated $9,550 for 2026).

✓ Step 5: Bridge Accounts for Early Retirement. Consider taxable brokerage accounts for funds you might need before age 59.5, or investigate Roth conversion ladders from Traditional IRAs to access funds after 5 years tax- and penalty-free.

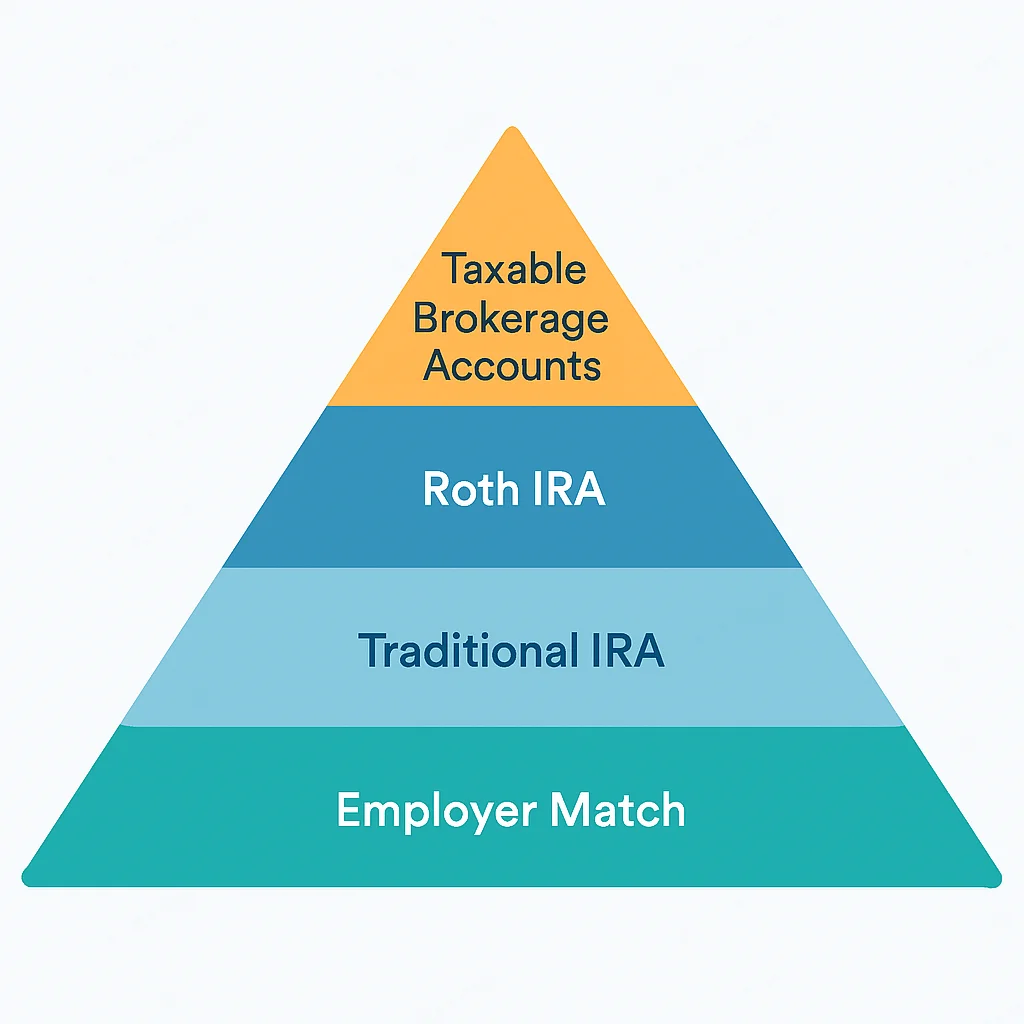

General Prioritization Strategy

When deciding where to put your money, follow this general hierarchy:

- Employer 401(k) up to the match: This is free money.

- HSA (if eligible): Triple tax advantage makes it a powerful retirement tool.

- Roth IRA (direct or backdoor): Tax-free growth and withdrawals are invaluable.

- Max out 401(k) (Trad or Roth): Leverage the full $23,500 (or $31,000 with catch-up) limit.

- Solo 401(k) (if self-employed): Maximize both employee and employer contributions.

- Mega Backdoor Roth (if available): For very high earners seeking more Roth space.

- Taxable Brokerage Account: For additional savings once tax-advantaged accounts are full.

KEY POINT

The ideal strategy involves a layered approach: secure the “free money” first, then prioritize tax-free growth (Roth accounts, HSA), and finally maximize tax-deferred options before moving to taxable accounts.

6. Important Caveats and Frequently Asked Questions (FAQ)

While the strategies outlined are powerful, it is crucial to understand the broader context and potential challenges.

Market Volatility and Investment Risk

Investing in the stock market carries inherent risks. While historical returns have been positive over the long term, there will be periods of volatility and downturns. Developers, especially those working for tech companies, might have a significant portion of their wealth tied to tech stocks (e.g., through RSUs, stock options, or company-specific investments in their 401(k)). It is important to diversify your investments beyond just your employer’s stock and across different asset classes (stocks, bonds, real estate) to mitigate risk.

Inflation and Purchasing Power

The cost of living tends to increase over time due to inflation. A million dollars today will have less purchasing power in 30 years. When planning your retirement, factor in inflation by aiming for a higher target nest egg or by using inflation-adjusted return rates in your calculations. Historically, inflation averages around 2-3% annually, but it can fluctuate significantly.

Tax Law Changes

Tax laws are subject to change by Congress. While the core principles of 401(k)s and IRAs have remained stable, contribution limits, income phase-outs, and specific rules (like those governing backdoor Roth conversions) can be modified. Stay informed about legislative changes that could impact your retirement planning strategies. The contribution limits for 2026 mentioned in this article are based on current estimates and may be adjusted by the IRS later in 2025.

Importance of Professional Advice

While this guide provides a comprehensive overview, personal financial situations vary greatly. Complex scenarios involving RSUs, stock options, multiple income streams, or specific early retirement goals often benefit from professional guidance. A fee-only financial advisor can help you create a personalized plan, optimize your investments, and navigate tax complexities. A qualified tax professional can ensure you are correctly reporting contributions and conversions.

WARNING

Always verify current IRS contribution limits and income thresholds for 2026 once they are officially released. The figures provided in this article are estimates based on historical adjustments and are subject to change.

Frequently Asked Questions (FAQ)

Q. What are the key differences between a Traditional 401(k) and a Roth 401(k)?

A Traditional 401(k) uses pre-tax contributions, reducing your current taxable income, with withdrawals taxed in retirement. A Roth 401(k) uses after-tax contributions, meaning no upfront tax break, but qualified withdrawals in retirement are completely tax-free. The choice depends on whether you expect to be in a higher or lower tax bracket now versus in retirement.

Q. Can I contribute to both an employer 401(k) and a Solo 401(k) in 2026?

Yes, you can. You can contribute as an employee to your employer’s 401(k) and also contribute to a Solo 401(k) based on your self-employment income. The employee contribution limit (estimated $23,500 for 2026) is shared across all 401(k)s, but you can also make employer contributions to your Solo 401(k) up to its separate limit, allowing for significant overall savings.

Q. What is the “pro-rata rule” for backdoor Roth IRAs, and how can I avoid it?

The “pro-rata rule” states that if you have any pre-tax money in any Traditional, SEP, or SIMPLE IRAs when you perform a Roth conversion, a portion of your conversion will be taxable. To avoid this, you should roll over any existing pre-tax IRA balances into your employer’s 401(k) (if allowed) before executing the backdoor Roth strategy, ensuring your Traditional IRA balance is zero.

Q. How much should I aim to save for retirement as a developer?

A common guideline is to save 10-15% of your income, but for developers with higher incomes and potential early retirement goals, aiming for 20% or more is often recommended. Many financial experts suggest having 1x your salary saved by age 30, 3x by 40, 6x by 50, and 8x by 60. However, personalized goals and expenses should drive your specific target.

7. Wrap-Up: Secure Your Future, Starting Today

Retirement planning might seem complex, but by understanding and diligently applying the strategies for your 401(k), Roth IRA, and Solo 401(k) in 2026, you can build a robust financial future. As a developer, your high earning potential is a powerful asset; do not let it go to waste by neglecting strategic savings.

Remember the core principles: start early, contribute consistently, maximize employer matches, leverage Roth accounts for tax-free growth, and explore advanced strategies like the backdoor Roth or Solo 401(k) when applicable. Regularly review your investments, adjust your contributions as your income grows, and seek professional advice for personalized guidance. Your future self will thank you for the financial discipline you cultivate today.

Thanks for reading, Kwonglish

We hope this guide empowers you to take control of your retirement planning. The journey to financial independence is a marathon, not a sprint, and every contribution counts.

Got questions or your own developer retirement tips? Drop a comment below!