SUMMARY

Investing 101 for Developers: Your Beginner’s Guide to Building Wealth in 2026

This is a friendly guide to fundamental investing principles for developers, covering stocks, ETFs, mutual funds, and how to start building your financial future.

Keywords: Investing, Personal Finance, Wealth Building

TABLE OF CONTENTS

1. Why Investing is a Must for Developers in 2026

2. Understanding Core Investment Vehicles

3. Crafting Your Developer Investment Strategy

4. Getting Started: Your First Investment Steps

5. Common Pitfalls and Smart Practices

6. Frequently Asked Questions (FAQ)

OVERVIEW

Why Investing is a Must for Developers in 2026

Hello, fellow developers! Kwonglish here. We spend our days creating amazing software, solving complex problems, and constantly learning new technologies. But how much time do we dedicate to building our own financial future? If you’re like many in the tech world, your salary might be good, but understanding how to make that money work for you can feel like learning a whole new programming language – intimidating at first, but incredibly powerful once you grasp the fundamentals.

In 2026, the financial landscape continues to evolve, but the core principles of wealth building remain steadfast. For developers, with generally stable and higher-than-average incomes, the opportunity to invest early and consistently is immense. This guide is designed to cut through the jargon and give you a practical, actionable roadmap to start investing, whether you’re fresh out of bootcamp or have years of experience under your belt. Think of it as your first commit to financial independence!

The goal isn’t to turn you into a day trader or a financial guru overnight. It’s about empowering you with the knowledge to make informed decisions, leverage compound interest – arguably the eighth wonder of the world – and build a secure future. We’ll cover the basics of common investment vehicles, strategies for getting started, and even some pitfalls to avoid. Let’s dive in and start coding your financial success!

KEY POINT

Starting early is the single most powerful advantage in investing. Even small, consistent contributions can grow into substantial wealth over time thanks to the magic of compound interest. Don’t wait until you “know everything” – start with the basics and learn as you go.

CORE GUIDE

Understanding Core Investment Vehicles

Before you can build an investment portfolio, you need to understand the fundamental building blocks. Here, we’ll break down the most common investment vehicles accessible to beginners: stocks, Exchange-Traded Funds (ETFs), and mutual funds.

1. Stocks: Owning a Piece of the Company

When you buy a stock, you’re purchasing a small ownership share in a public company. If the company performs well, its value can increase, and so can the price of your stock. Some companies also pay dividends, which are distributions of a portion of their earnings to shareholders.

Stocks: Pros & Cons

Pros — Potentially high returns, direct ownership in companies you believe in, dividend income.

Cons — Higher risk (company-specific), requires research, can be volatile.

As a developer, you might naturally gravitate towards tech stocks like Apple, Microsoft, or Google’s parent company, Alphabet. While these have historically performed well, remember that putting all your eggs in one basket, even a tech basket, is risky. A single bad quarter or a new competitor could significantly impact your investment. For beginners, focusing on individual stocks might be too high-risk without proper diversification, which we’ll discuss shortly.

2. Exchange-Traded Funds (ETFs): Instant Diversification

ETFs are like baskets of various investments – they can hold stocks, bonds, commodities, or a mix of these. When you buy an ETF, you’re essentially buying a share of that basket. The beauty of ETFs is that they offer instant diversification. Instead of buying one share of Apple, you could buy one share of an ETF that holds hundreds of different tech companies, or even the entire S&P 500 index.

ETFs: Pros & Cons

Pros — High diversification, low expense ratios (fees), traded like stocks throughout the day, tax-efficient.

Cons — Can have trading costs (commissions, though many brokers offer commission-free ETFs), price can fluctuate intraday.

For beginners, ETFs that track broad market indexes are often recommended. Examples include VOO (Vanguard S&P 500 ETF), which tracks the performance of the 500 largest U.S. companies, or QQQ (Invesco QQQ Trust), which tracks the NASDAQ 100 (primarily large tech companies). These offer broad market exposure with minimal effort.

KEY POINT

ETFs are an excellent starting point for beginners due to their inherent diversification and typically low costs. They allow you to invest in a wide range of companies or sectors without having to research and buy individual stocks.

3. Mutual Funds: Professionally Managed Portfolios

Similar to ETFs, mutual funds pool money from many investors to purchase a diversified portfolio of stocks, bonds, or other securities. The key difference is that mutual funds are actively managed by a fund manager who makes decisions about buying and selling assets within the fund. They are priced once a day after the market closes.

Mutual Funds: Pros & Cons

Pros — Professional management, broad diversification, often good for target-date retirement funds.

Cons — Higher expense ratios (fees) due to active management, less tax-efficient than ETFs, only traded once a day, can have minimum investment requirements (e.g., $1,000 to $3,000).

While active management sounds appealing, studies have consistently shown that most actively managed mutual funds fail to outperform their benchmark index (like the S&P 500) over the long term, especially after accounting for their higher fees. For this reason, many financial advisors recommend low-cost index funds (a type of mutual fund that passively tracks an index) or ETFs over actively managed mutual funds for most investors.

ETFs vs. Mutual Funds: A Quick Comparison

Here’s a quick side-by-side to help you decide which might be better for your current investment style:

Key Differences

Trading: ETFs trade like stocks throughout the day; Mutual Funds are priced once daily.

Management: ETFs can be active or passive (most popular are passive); Mutual Funds are typically active.

Costs: ETFs generally have lower expense ratios; Mutual Funds often have higher fees due to active management.

Minimums: ETFs typically have no minimum beyond share price; Mutual Funds often have minimum investments (e.g., $1,000+).

CORE GUIDE

Crafting Your Developer Investment Strategy

Just like you wouldn’t start coding without a plan, you shouldn’t start investing without a strategy. Here’s how to build one that aligns with your financial goals and risk tolerance.

1. Define Your Financial Goals

What are you investing for? Your goals will dictate your timeline and risk appetite. Common goals include:

Short-term (1-3 years): Emergency fund (3-6 months of expenses in a high-yield savings account), down payment for a house in 2026 or 2027, new car. For these, low-risk options like savings accounts or Certificates of Deposit (CDs) are usually best, as the stock market is too volatile for short timelines.

Medium-term (3-10 years): Child’s education, significant home renovations. A balanced portfolio of stocks and bonds might be suitable here.

Long-term (10+ years): Retirement, financial independence. This is where the stock market truly shines, allowing compound interest to work its magic. A growth-oriented portfolio with a higher allocation to stocks/ETFs is typical.

2. Assess Your Risk Tolerance

How comfortable are you with the value of your investments going up and down? This is your risk tolerance. As a developer, you might be used to logical, predictable systems. The market is anything but. It’s crucial to be honest with yourself. If a 10-20% drop in your portfolio would cause sleepless nights, you might have a lower risk tolerance than someone who sees it as a “sale.”

Generally, younger investors with a long time horizon (20+ years until retirement) can afford to take on more risk, as they have time to recover from market downturns. As you get closer to your goals, you typically de-risk your portfolio by shifting more money into less volatile assets like bonds.

3. Diversification: Don’t Put All Your Eggs in One Basket

Diversification means spreading your investments across different asset classes (stocks, bonds, real estate), industries, and geographies. This helps reduce risk. If one part of your portfolio performs poorly, another might perform well, balancing things out. This is why broad market ETFs are so popular – they provide instant diversification.

KEY POINT

For most beginner investors, a simple, diversified portfolio of low-cost index funds or ETFs (e.g., 70% total stock market ETF, 30% total bond market ETF) is often sufficient to achieve long-term growth and outperform many actively managed funds.

4. Dollar-Cost Averaging (DCA): The Consistent Approach

Dollar-cost averaging is an investment strategy where you invest a fixed amount of money at regular intervals (e.g., $200 every two weeks) regardless of the asset’s price. This strategy reduces the impact of volatility. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more shares. Over time, your average cost per share tends to be lower than if you tried to time the market (which is notoriously difficult, even for pros).

As developers, we love automation. DCA is the financial equivalent – set it and forget it! Most brokerage accounts allow you to set up automatic recurring investments, making DCA effortless.

REAL-WORLD EXAMPLES

Getting Started: Your First Investment Steps

You’ve got the foundational knowledge. Now, let’s talk about taking action. Here’s a practical guide to making your first investment in 2026.

1. Choose the Right Investment Account

The first step is opening an investment account. You have a few main options:

Employer-Sponsored Retirement Plans (e.g., 401(k), 403(b)): If your employer offers one, this is often the best place to start, especially if they provide a matching contribution. That’s essentially free money! Contribute at least enough to get the full match. These are tax-advantaged accounts, meaning your investments grow tax-deferred or tax-free (in a Roth 401(k)).

Individual Retirement Accounts (IRAs – Traditional or Roth): These are personal retirement accounts you open yourself. In 2026, the contribution limit for IRAs is typically around $7,000 (check current IRS guidelines). Roth IRAs are great for developers who expect to be in a higher tax bracket in retirement, as contributions are after-tax but qualified withdrawals are tax-free.

Taxable Brokerage Accounts: After maximizing your tax-advantaged accounts, you can open a standard brokerage account. These offer more flexibility (no withdrawal age restrictions) but investments are subject to capital gains taxes.

Health Savings Accounts (HSAs): If you have a high-deductible health plan (HDHP), an HSA is a triple-tax-advantaged account: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Many HSAs allow you to invest funds beyond a certain cash threshold.

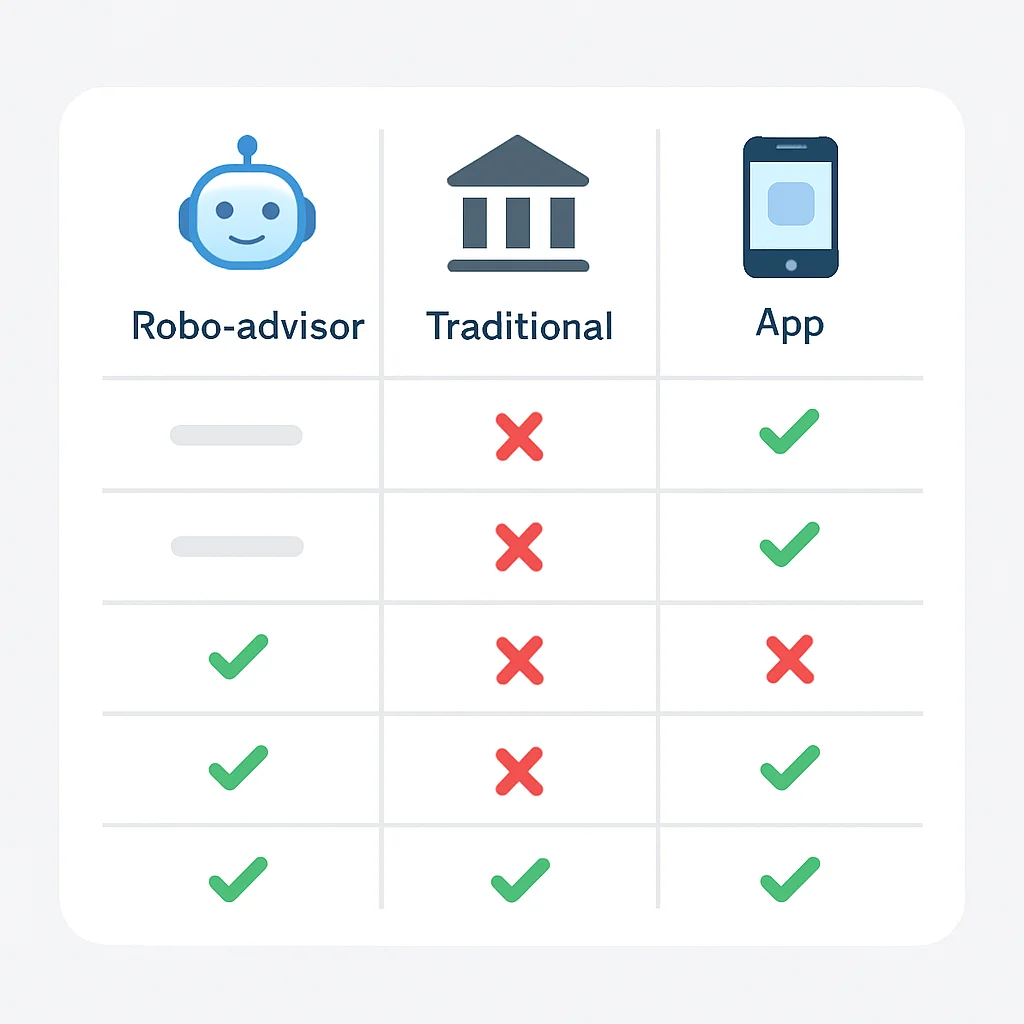

2. Choose a Brokerage Platform

Several platforms cater to different needs:

Traditional Brokerages (e.g., Fidelity, Vanguard, Charles Schwab): Offer a wide range of investment products, research tools, and customer support. Great for those who want more control.

Robo-Advisors (e.g., Betterment, Wealthfront): These platforms use algorithms to build and manage diversified portfolios based on your risk tolerance and goals. They’re excellent for beginners who want a hands-off approach, typically charging a small annual fee (e.g., 0.25% of assets under management).

Commission-Free Trading Apps (e.g., Robinhood, Webull): While popular, these often encourage more frequent trading and might not be ideal for a long-term, buy-and-hold strategy for beginners. Use with caution.

3. Your First Investment: A Step-by-Step Example

Let’s say you’ve decided to open a Roth IRA with Vanguard and invest in a total stock market ETF (like VTI) and a total bond market ETF (like BND).

1

Open and Fund Your Account

Complete the online application for your chosen brokerage. Once approved, link your bank account and transfer funds. For a Roth IRA in 2026, you might aim to contribute the maximum $7,000 for the year, or start with a smaller amount like $500.

2

Research and Select Your Investments

Log in to your account. Use the search function to find VTI (Vanguard Total Stock Market ETF) and BND (Vanguard Total Bond Market ETF). Review their expense ratios (VTI: ~0.03%, BND: ~0.035%) and holdings. For a long-term, moderate-risk portfolio, a common allocation is 80% stocks / 20% bonds.

3

Place Your Buy Order

If you transferred $1,000, you might allocate $800 to VTI and $200 to BND. Enter a “market order” to buy shares immediately at the current price, or a “limit order” if you want to specify a maximum price you’re willing to pay. For long-term investing in highly liquid ETFs, a market order is generally fine.

4

Set Up Recurring Investments

This is where DCA comes in. Set up an automatic transfer of a fixed amount (e.g., $100 or $200) from your checking account to your Roth IRA every payday or once a month. Then, set up automatic investments within your Roth IRA to buy more VTI and BND in your chosen allocation.

Congratulations! You’ve made your first investment. Now, the key is consistency and patience.

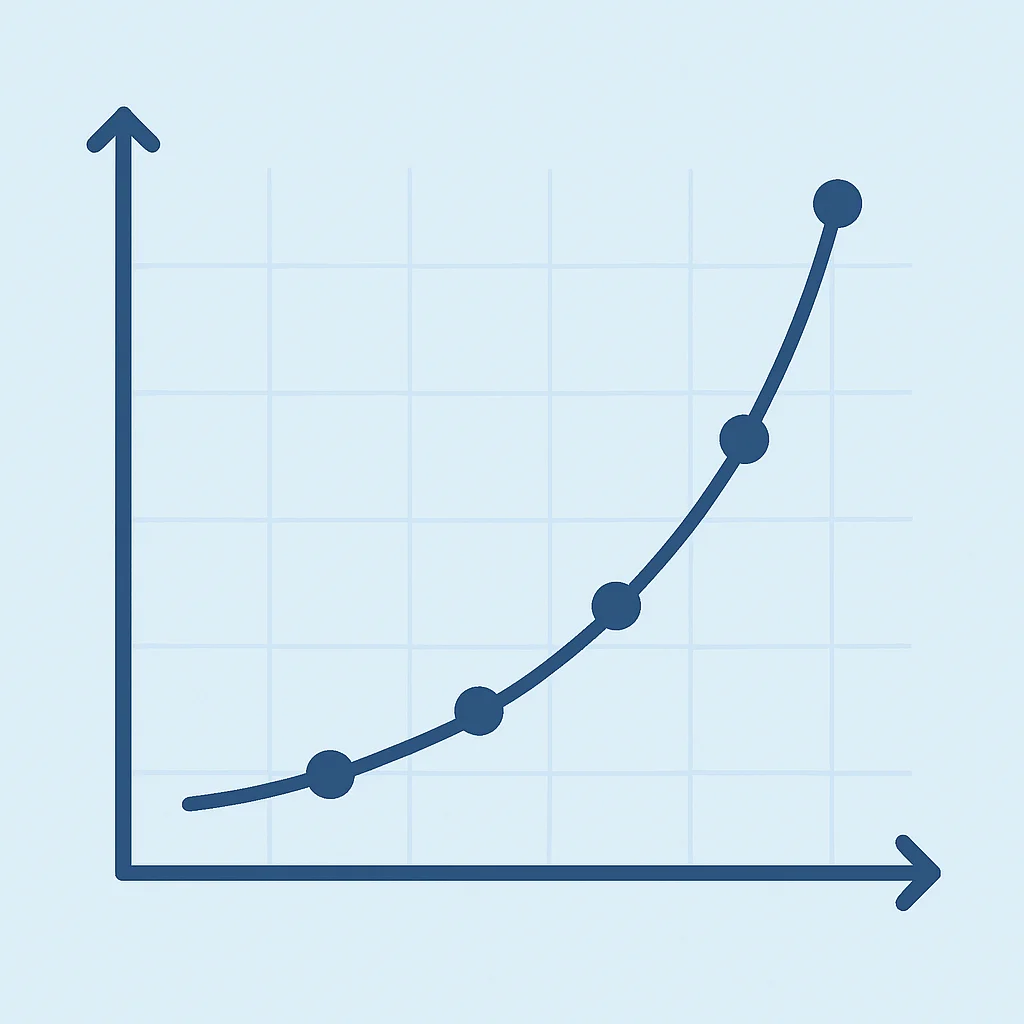

Understanding Compound Interest with Code

As developers, we appreciate how algorithms work. Let’s visualize compound interest with a simple Python snippet. This demonstrates how your money grows not just on your initial investment, but also on the interest earned in previous periods.

CODE EXPLANATION

This Python code calculates the future value of an investment with a fixed annual return over a specified number of years, demonstrating the power of compound interest without additional contributions.

def calculate_compound_interest(principal, annual_rate, years):

"""

Calculates the future value of an investment with compound interest.

Args:

principal (float): The initial amount of money invested.

annual_rate (float): The annual interest rate (e.g., 0.07 for 7%).

years (int): The number of years the money is invested.

Returns:

float: The future value of the investment.

"""

future_value = principal * (1 + annual_rate)**years

return future_value

initial_investment = 10000 # $10,000

average_annual_return = 0.07 # 7% average annual return

investment_years = 30 # Invest for 30 years

final_amount = calculate_compound_interest(initial_investment, average_annual_return, investment_years)

print(f"Initial Investment: ${initial_investment:,.2f}")

print(f"Annual Return: {average_annual_return*100}%")

print(f"Investment Period: {investment_years} years")

print(f"Future Value after {investment_years} years: ${final_amount:,.2f}")

# Example with different years to show growth

print("\nGrowth over different periods:")

for y in range(5, investment_years + 1, 5):

amount_at_y = calculate_compound_interest(initial_investment, average_annual_return, y)

print(f" After {y} years: ${amount_at_y:,.2f}")

CODE EXPLANATION

Running this code will show you that an initial $10,000 investment at a 7% annual return can grow to over $76,000 in 30 years. Imagine adding to that regularly! This doesn’t even account for additional contributions, which would make the growth even more dramatic.

This simple model highlights why time in the market is more important than timing the market. The longer your money is invested, the more time it has to compound.

CAVEATS + FAQ

Common Pitfalls and Smart Practices

Investing isn’t without its challenges. Being aware of common mistakes can help you navigate the market more successfully.

WARNING

Don’t try to time the market: Nobody, not even professional investors, can consistently predict market tops and bottoms. Focus on time in the market, not timing the market.

WARNING

Avoid excessive trading: Frequent buying and selling often leads to higher transaction costs and can trigger more capital gains taxes, eroding your returns. A long-term, buy-and-hold strategy is generally more effective for wealth building.

WARNING

Don’t panic sell during downturns: Market corrections are a normal part of investing. Selling when the market is down locks in losses. Historically, markets recover and reach new highs. Stick to your plan and potentially even invest more (dollar-cost averaging) during dips.

KEY POINT

Always prioritize your emergency fund (3-6 months of living expenses in cash) before investing in the stock market. This provides a crucial safety net for unexpected events without having to sell investments at a loss.

Disclaimer: I am not a financial advisor. This content is for informational and educational purposes only and does not constitute financial advice. Always consult with a qualified financial professional before making any investment decisions. Investment involves risk, including the possible loss of principal.

Frequently Asked Questions (FAQ)

Q. How much money do I need to start investing in 2026?

You can start investing with very little money, even $5 or $10, through fractional shares offered by many modern brokerages. For ETFs, you’ll need enough to buy at least one share, which can range from $50 to $400+. Consistency is more important than the initial lump sum.

Q. Should I pay off my high-interest debt before investing?

Yes, generally. Debts with high interest rates (like credit card debt, often 18-25%+) typically outweigh potential investment returns. Focus on paying off such debts first, as it’s a guaranteed “return” equal to the interest rate you avoid paying.

Q. What’s a good average annual return to expect from the stock market?

Historically, the U.S. stock market (S&P 500) has returned an average of about 10-12% annually before inflation over long periods. However, past performance does not guarantee future results, and individual years can see significant fluctuations, both up and down.

Q. How often should I check my investment portfolio?

For long-term investors, checking your portfolio too frequently can lead to emotional decisions. It’s generally recommended to review your portfolio quarterly or semi-annually, focusing on your overall asset allocation and rebalancing if necessary, rather than daily price movements.

WRAP-UP

Your Journey to Financial Independence Starts Now

As a developer, you’re equipped with analytical skills, a knack for problem-solving, and often a solid income. These are incredibly powerful assets when applied to personal finance and investing. The most important lesson from this guide isn’t about picking the next hot stock; it’s about consistency, patience, and understanding the fundamental principles.

Start by automating your investments into broad, low-cost index funds or ETFs in tax-advantaged accounts. Embrace dollar-cost averaging. Don’t let market volatility scare you away from your long-term goals. Your financial journey, much like a complex software project, requires continuous learning, iteration, and disciplined execution. By taking these initial steps in 2026, you’re not just investing money; you’re investing in your future freedom and peace of mind.

Thanks for reading!

I hope this guide has demystified the world of investing for you. Remember, every financial expert started as a beginner.

Got feedback or questions? Drop a comment below! Let’s build wealth together.