SUMMARY

Smart Debt Management for Developers: Strategies to Pay Off Loans & Credit Cards in 2026

This is a practical guide for developers to effectively manage and pay off student loans and credit card debt, building a stronger financial future in 2026.

Keywords: debt management, student loans, credit card debt, personal finance

TABLE OF CONTENTS

1. Overview: Why Smart Debt Management Matters for Developers

2. Understanding Your Debt Landscape in 2026

3. Budgeting for Effective Debt Repayment

4. Proven Debt Repayment Strategies: Avalanche vs. Snowball

5. Advanced Debt Management Tactics

6. Building Your Financial Safety Net

7. Real-World Developer Debt Scenarios

8. Important Considerations & Caveats

9. Frequently Asked Questions (FAQ)

10. Wrap-Up: Your Path to Financial Freedom

1. Overview: Why Smart Debt Management Matters for Developers

Hello, Kwonglish readers! As developers, we often find ourselves in a favorable position regarding income potential. The demand for skilled tech professionals is on the rise, resulting in competitive salaries. However, a high income does not guarantee financial freedom. Many developers, particularly those early in their careers or those who have heavily invested in education, struggle with substantial student loan debt, and credit card balances can also accumulate. Neglecting these debts can significantly impede your financial growth, restrict future opportunities, and create unnecessary stress.

As we approach 2026, with changing economic conditions and interest rate variations, proactive debt management is more important than ever. The average student loan debt in the U.S. remains high, often surpassing $30,000 per borrower, while credit card interest rates can easily exceed 20%. These statistics underscore the urgency of implementing effective strategies. This guide is not solely about repaying loans; it is about establishing a robust financial foundation that enables you to invest, save for your future, and attain genuine financial independence. We will explore practical, actionable strategies tailored to the financial realities of developers, empowering you to manage your debt with confidence and precision. Let’s embark on the journey to simplify your financial life!

KEY POINT

A high income alone does not resolve debt issues. Strategic and proactive debt management in 2026 is crucial for developers to achieve lasting financial security and unlock future opportunities, particularly given the high average debt levels and interest rates.

2. Understanding Your Debt Landscape in 2026

Before you can tackle your debt, it is essential to understand precisely what you are facing. Think of it as debugging a complex system: you cannot fix a bug until you comprehend its root cause and implications. This initial step involves gathering data and creating a clear overview of your current financial obligations.

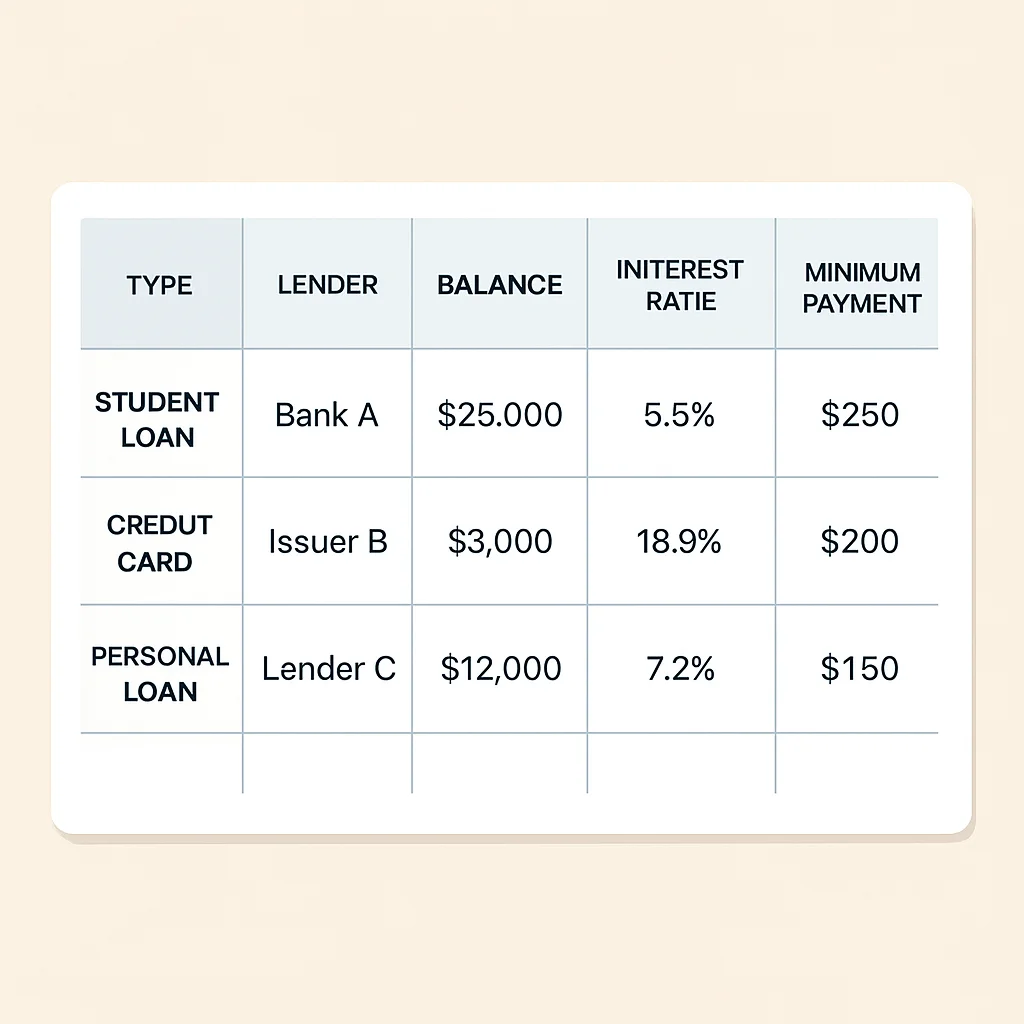

Inventory All Your Debts

Take a spreadsheet or a notebook and document every single debt you possess. Ensure nothing is overlooked! This includes:

✓ Student Loans: Federal (Stafford, Perkins, PLUS) and private loans. Be specific about each loan if you have multiple.

✓ Credit Cards: All open accounts, even those with small balances that may seem insignificant.

✓ Personal Loans: Any unsecured loans from banks or online lenders, often utilized for unexpected expenses.

✓ Car Loans: If applicable, though usually lower priority due to lower interest rates.

For each debt, record the following key details:

- Lender Name: The entity you owe money to (e.g., Sallie Mae, Chase, Discover).

- Current Balance: The exact amount you currently owe.

- Interest Rate (APR): This is critical! Note if it is fixed or variable. Credit card APRs can range from 15% to 30%+, while student loans might be 4% to 8%. This rate dictates how quickly your debt grows.

- Minimum Monthly Payment: The smallest amount you must pay each month to avoid late fees and negative credit reporting.

- Payment Due Date: To ensure you do not miss payments and incur additional fees.

- Loan Term Remaining: How many months or years until the loan is fully paid off (especially for student or car loans). This helps visualize the long-term commitment.

Once you have compiled all this information, you will start noticing patterns and identifying which debts are the most burdensome. High-interest credit card debt is typically the most urgent to address due to its rapid growth. For instance, a $5,000 credit card balance at 25% APR can accumulate over $100 in interest per month even if you make minimum payments, making it incredibly challenging to reduce the principal.

KEY POINT

The first step in effective debt management is a comprehensive inventory of all your loans, including lender, current balance, exact interest rate (APR), minimum payment, and remaining term. This data is your foundation for strategic planning, revealing which debts are most costly.

3. Budgeting for Effective Debt Repayment

With your debt inventory completed, the next vital step is to comprehend your cash flow. A budget is not about restricting yourself; it is about assigning every dollar a purpose and ensuring you have enough resources to confront your debts directly. Many developers earn good salaries, but without a budget, that money can easily vanish into lifestyle inflation or unforeseen expenses, leaving little for aggressive debt repayment.

Creating Your Developer-Friendly Budget

Begin by tracking your income and expenses for at least one month, ideally two or three, to gain an accurate understanding of your spending habits. Many budgeting apps (like Mint, YNAB, or even a simple spreadsheet) can help automate this process by linking to your bank accounts and categorizing transactions. Categorize everything:

- Fixed Expenses: These generally remain the same each month. Consider rent/mortgage, minimum debt payments, insurance premiums, essential software subscriptions (e.g., IDE licenses, cloud services for personal projects), and utility bills.

- Variable Expenses: These fluctuate monthly. Common examples include groceries, dining out, entertainment, transportation (gas, public transit), clothing, and personal care items. This category often holds the most potential for savings.

- Savings Goals: Even while in debt, it is wise to allocate a small portion to an emergency fund and perhaps minimum contributions to retirement, especially if there is an employer match.

Once you have a clear overview, identify where your money is actually going. Developers often have specific expenses like professional development courses (e.g., Udemy, Coursera), conference tickets, or subscriptions to development tools and services (e.g., GitHub Copilot, prototyping tools). While many of these are valuable investments in your career, it is crucial to differentiate between essential and discretionary spending when you are in debt repayment mode. For example, a new course might be postponed if you have a 25% APR credit card balance.

Finding Extra Cash for Debt

The goal here is to free up as much money as possible to direct towards your debt beyond the minimum payments. Look for areas to cut back without significantly affecting your quality of life:

- Review Subscriptions: Are you still utilizing all those streaming services (Netflix, Hulu, HBO Max), gym memberships, or even dormant SaaS subscriptions for side projects that you started and abandoned? Cancel what you do not actively use. A typical developer might save $50-100 a month here by being ruthless.

- Cut Down on Dining Out/Delivery: This is a common money drain. Eating out just three times a week can easily cost $150-$200. Cooking at home even a few more times a week can save hundreds of dollars each month. Plan your meals!

- Transportation: Can you bike, walk, or use public transport more often? If you own a car, consider carpooling or combining errands to save on gas.

- Side Hustles: As a developer, your skills are highly marketable. Freelancing on platforms like Upwork or Fiverr, tutoring coding, or building a small app or website for a local business can generate significant extra income. Even an additional $500-$1000 a month from a few hours of work can dramatically accelerate debt repayment. Think about creating a small SaaS product or offering technical consulting.

KEY POINT

A detailed budget reveals where your money goes and where you can find extra cash for debt repayment. Developers can leverage their specialized skills for side income and critically evaluate tech-related subscriptions to free up substantial funds.

4. Proven Debt Repayment Strategies: Avalanche vs. Snowball

Once you understand your debts and have a budget, it is time to select your repayment strategy. The two most popular and effective methods are the Debt Avalanche and Debt Snowball. Both approaches involve paying the minimum on all debts except one, on which you focus all your extra payments.

The Debt Avalanche Method (Mathematical Approach)

This method prioritizes paying off debts with the highest interest rate first. After paying the minimum on all other debts, you direct all your extra available cash towards the debt with the highest APR. Once that debt is settled, you take the money you were paying on it (its minimum payment plus all the extra money you were applying) and apply it to the next highest interest rate debt. This snowballing of payments continues until all debts are eliminated, similar to an avalanche gaining size.

Why it works: Mathematically, the Debt Avalanche method saves you the most money on interest over time. By eliminating the most expensive debts first, you reduce the total amount of interest you will pay, making it the most efficient way to escape debt financially. This method requires discipline but yields the greatest monetary savings.

Example Scenario:

Let’s say you have an extra $500 per month from your developer salary after minimum payments and essential expenses:

- Credit Card A: $5,000 balance, 24% APR, $100 min payment

- Credit Card B: $2,000 balance, 18% APR, $50 min payment

- Student Loan: $20,000 balance, 6% APR, $200 min payment

With the Avalanche method, you would pay the minimums on CC B ($50) and Student Loan ($200). Then, you would direct your $500 extra + CC A’s minimum payment ($100) = $600 towards Credit Card A. Once CC A is paid off, you would take that $600 (which was going to CC A) and add it to CC B’s minimum payment ($50), sending a total of $650 to CC B. This continues until all debts are cleared. This approach ensures you tackle the most financially draining debts first.

CODE EXPLANATION

This Python-like pseudocode illustrates the basic logic of the Debt Avalanche method. It sorts debts by interest rate in descending order and iteratively applies extra payments to the highest interest debt. The current_extra_payment_pool accumulates the minimum payments from paid-off debts, which are then redirected to the next target debt, creating the “avalanche” effect.

function calculate_avalanche_repayment(debts, extra_payment_per_month):

// debts is a list of objects: [{name, balance, interest_rate, min_payment}]

// Sort debts by interest_rate in descending order to prioritize highest APR

sorted_debts = sort(debts, key=lambda d: d.interest_rate, reverse=True)

total_months = 0

payments_log = []

// Create a deep copy to avoid modifying original debt objects

current_debts = [d.copy() for d in sorted_debts]

while any(d.balance > 0 for d in current_debts):

total_months += 1

current_extra_payment_pool = extra_payment_per_month

monthly_payments_made = {}

// Identify the current debt to focus extra payments on

focus_debt_index = 0

while focus_debt_index < len(current_debts) and current_debts[focus_debt_index].balance <= 0:

focus_debt_index += 1

if focus_debt_index >= len(current_debts): // All debts paid

break

for i, debt in enumerate(current_debts):

if debt.balance > 0:

// Calculate and add interest for the month

monthly_interest = debt.balance * (debt.interest_rate / 12 / 100)

debt.balance += monthly_interest

// Determine payment for this month (minimum or remaining balance)

payment_this_month = debt.min_payment

if debt.balance < payment_this_month:

payment_this_month = debt.balance // Pay remaining balance

// Make the payment

debt.balance -= payment_this_month

monthly_payments_made[debt.name] = payment_this_month

// If this is the focus debt, apply any available extra payment

if i == focus_debt_index and current_extra_payment_pool > 0:

extra_to_apply = min(current_extra_payment_pool, debt.balance)

debt.balance -= extra_to_apply

monthly_payments_made[debt.name] += extra_to_apply

current_extra_payment_pool -= extra_to_apply

if debt.balance <= 0:

debt.balance = 0 // Ensure balance doesn't go negative

// If a debt is paid off, its previous payment amount is added to the extra pool

// for the next highest interest debt.

if i == focus_debt_index:

current_extra_payment_pool += monthly_payments_made[debt.name] // Add its total payment to the pool

payments_log.append({"month": total_months, "balances": {d.name: d.balance for d in current_debts}})

// Safety break for extremely long repayment scenarios

if total_months > 600: // More than 50 years, likely an issue or very small payments

print("Warning: Repayment exceeding 50 years. Check parameters.")

break

return {"months_to_pay_off": total_months, "log": payments_log}

// Example usage (assuming 'debts' is defined as a list of dictionaries/objects):

// debts = [

// {"name": "CC A", "balance": 5000, "interest_rate": 24, "min_payment": 100},

// {"name": "CC B", "balance": 2000, "interest_rate": 18, "min_payment": 50},

// {"name": "Student Loan", "balance": 20000, "interest_rate": 6, "min_payment": 200}

// ]

// result = calculate_avalanche_repayment(debts, 500)

// print(result)

The Debt Snowball Method (Psychological Approach)

The Debt Snowball method focuses on paying off debts with the smallest balance first, regardless of the interest rate. You pay the minimum on all debts except the one with the smallest balance, to which you apply all your extra payments. Once that smallest debt is eliminated, you take the money you were paying on it (its minimum payment plus all the extra money you were applying) and apply it to the next smallest debt. This builds momentum, like a snowball rolling downhill and gathering size and speed.

Why it works: While it might cost slightly more in interest over time compared to the Avalanche method, the Debt Snowball method provides powerful psychological wins. Quickly eliminating small debts gives you a boost of motivation and a sense of accomplishment to keep going, which can be crucial for long-term adherence to a debt repayment plan, especially if you feel overwhelmed by large balances.

Example Scenario:

Using the same debts and $500 extra per month:

- Credit Card A: $5,000 balance, 24% APR, $100 min payment

- Credit Card B: $2,000 balance, 18% APR, $50 min payment

- Student Loan: $20,000 balance, 6% APR, $200 min payment

With the Snowball method, you would pay the minimums on CC A ($100) and Student Loan ($200). Then, you would direct your $500 extra + CC B’s minimum payment ($50) = $550 towards Credit Card B (the smallest balance). Once CC B is paid off, you would take that $550 (which was going to CC B) and add it to CC A’s minimum payment ($100), sending a total of $650 to CC A. This continues until all debts are cleared. This method focuses on building momentum and celebrating milestones.

CODE EXPLANATION

This Python-like pseudocode outlines the Debt Snowball strategy. Debts are sorted by balance in ascending order, and extra payments are focused on the smallest debt first. Similar to the Avalanche, the current_extra_payment_pool ensures that all funds freed up from a paid-off debt are rolled into the next target debt.

function calculate_snowball_repayment(debts, extra_payment_per_month):

// debts is a list of objects: [{name, balance, interest_rate, min_payment}]

// Sort debts by balance in ascending order to prioritize smallest balances

sorted_debts = sort(debts, key=lambda d: d.balance)

total_months = 0

payments_log = []

current_debts = [d.copy() for d in sorted_debts]

while any(d.balance > 0 for d in current_debts):

total_months += 1

current_extra_payment_pool = extra_payment_per_month

monthly_payments_made = {}

// Identify the current debt to focus extra payments on

focus_debt_index = 0

while focus_debt_index < len(current_debts) and current_debts[focus_debt_index].balance <= 0:

focus_debt_index += 1

if focus_debt_index >= len(current_debts): // All debts paid

break

for i, debt in enumerate(current_debts):

if debt.balance > 0:

// Calculate and add interest for the month

monthly_interest = debt.balance * (debt.interest_rate / 12 / 100)

debt.balance += monthly_interest

// Determine payment for this month (minimum or remaining balance)

payment_this_month = debt.min_payment

if debt.balance < payment_this_month:

payment_this_month = debt.balance

// Make the payment

debt.balance -= payment_this_month

monthly_payments_made[debt.name] = payment_this_month

// If this is the focus debt, apply any available extra payment

if i == focus_debt_index and current_extra_payment_pool > 0:

extra_to_apply = min(current_extra_payment_pool, debt.balance)

debt.balance -= extra_to_apply

monthly_payments_made[debt.name] += extra_to_apply

current_extra_payment_pool -= extra_to_apply

if debt.balance <= 0:

debt.balance = 0

if i == focus_debt_index:

current_extra_payment_pool += monthly_payments_made[debt.name]

payments_log.append({"month": total_months, "balances": {d.name: d.balance for d in current_debts}})

if total_months > 600:

print("Warning: Repayment exceeding 50 years. Check parameters.")

break

return {"months_to_pay_off": total_months, "log": payments_log}

// Example usage:

// debts = [

// {"name": "CC A", "balance": 5000, "interest_rate": 24, "min_payment": 100},

// {"name": "CC B", "balance": 2000, "interest_rate": 18, "min_payment": 50},

// {"name": "Student Loan", "balance": 20000, "interest_rate": 6, "min_payment": 200}

// ]

// result = calculate_snowball_repayment(debts, 500)

// print(result)

KEY POINT

Choose between the Debt Avalanche (highest interest first for maximum monetary savings) and Debt Snowball (smallest balance first for powerful psychological motivation). Both are effective when consistently applied with extra payments.

5. Advanced Debt Management Tactics

Beyond the core repayment strategies, there are several other powerful tools developers can utilize to optimize their debt management in 2026, especially for high-interest credit card debt and student loans. These tactics can significantly reduce the total cost and time of your debt journey.

Balance Transfers for Credit Cards

If you have high-interest credit card debt, a 0% APR balance transfer credit card can be a game-changer. These cards offer an introductory period (typically 12 to 21 months) with no interest on transferred balances. This provides you with a crucial window to pay down the principal without new interest accumulating, effectively pausing the interest clock.

- Pros: Significant interest savings, a clear deadline for repayment, potentially lower monthly payments during the introductory period as all your payment goes directly to the principal. This can save you hundreds or even thousands on a large balance.

- Cons: Most cards charge a balance transfer fee (usually 3-5% of the transferred amount), which can add to your initial debt. For example, transferring $10,000 might incur a $300-$500 fee. If you do not pay off the balance before the 0% APR period ends, the remaining balance will be subject to a much higher standard APR, often 18-25%+. You also need a good to excellent credit score (typically 670+) to qualify for the best offers.

- Choosing a Card: Look for the longest 0% APR period and the lowest balance transfer fee. Read the fine print carefully, especially regarding the post-introductory APR and any annual fees.

WARNING

Do NOT use the new balance transfer card for new purchases. Focus exclusively on paying off the transferred balance aggressively within the 0% APR period. If you carry a balance past the introductory period, the high standard APR will kick in, potentially worsening your situation.

Student Loan Refinancing and Consolidation

For student loans, especially private ones, refinancing can be highly beneficial. Refinancing involves taking out a new loan from a private lender to pay off your existing student loans. If you have a strong credit score (700+), a stable developer income, and a low debt-to-income ratio, you might qualify for a significantly lower interest rate, which can save you thousands over the life of the loan. You might also be able to choose a shorter (faster repayment) or longer (lower monthly payment) repayment term.

- Federal vs. Private Loan Refinancing: This is a critical distinction. Refinancing federal student loans into a private loan means giving up valuable federal protections like income-driven repayment plans (which adjust payments based on your income), deferment, forbearance (allowing temporary payment pauses during hardship), and potential loan forgiveness programs (like Public Service Loan Forgiveness). Carefully weigh these benefits against potential interest savings. Refinancing private loans typically carries fewer risks to protections, as private loans generally do not offer the same safety nets.

- Federal Loan Consolidation: This is different from refinancing. Federal student loan consolidation combines multiple federal loans into one new federal loan, simplifying payments and potentially offering a fixed interest rate based on the weighted average of your original loans. It does not typically lower your interest rate but can extend your repayment term, which lowers monthly payments but increases total interest paid. This is done through the U.S. Department of Education.

Negotiating with Creditors

If you are genuinely struggling to make minimum payments due to job loss, illness, or other severe hardship, do not ignore the situation. Reach out to your creditors proactively. They may be willing to work with you to create a more manageable payment plan, temporarily reduce interest rates, or even settle for a lower lump-sum payment if you are in severe hardship. This is often a last resort before debt consolidation services or bankruptcy, but it is worth exploring before things worsen and negatively impact your credit score. Be honest about your financial situation and be prepared with documentation.

KEY POINT

Utilize balance transfers for credit cards (with careful planning and a repayment strategy) and consider refinancing student loans if you have a strong financial profile and fully understand the trade-offs, especially concerning federal loan protections.

6. Building Your Financial Safety Net

While aggressively paying down debt is important, it is equally crucial not to neglect building a financial safety net. Without an emergency fund, any unexpected expense – such as a car repair costing $800, a medical bill of $2,000, or even a temporary job loss – can derail your debt repayment progress and force you back into high-interest debt, creating a vicious cycle.

The Power of an Emergency Fund

An emergency fund is a stash of readily accessible cash (typically in a high-yield savings account, offering 4-5% APY in 2026) specifically for unforeseen circumstances. Financial experts generally recommend having 3 to 6 months’ worth of essential living expenses saved. For a developer earning a good salary, if your monthly expenses are $3,500, this means having $10,500 to $21,000 saved. This might seem like a large sum, but it provides immense peace of mind and prevents new debt from forming.

How to build it alongside debt repayment:

- Small Starter Fund: Aim for a mini-emergency fund of $1,000 to $2,000 first. This can cover most minor emergencies (e.g., a flat tire, a deductible) without resorting to credit cards. This is a non-negotiable first step before aggressive debt repayment.

- Hybrid Approach: Some financial advisors suggest a “debt first, then emergency fund” approach, while others advocate for building both simultaneously. A balanced approach is often best: get your small starter fund ($1,000-$2,000), then focus heavily on high-interest debt, while still contributing a smaller, consistent amount (e.g., $50-$100) to your full emergency fund each month. Once high-interest debt is eliminated, pivot to fully funding the emergency fund.

- Automate Savings: Set up an automatic transfer from your checking account to your high-yield savings account each payday. Even $50-$100 a month adds up quickly and ensures you are consistently saving without having to think about it. Treat it like another bill.

WARNING

Do not use your emergency fund for non-emergencies (e.g., a new gadget, vacation, down payment on a house). Its purpose is strictly for unforeseen financial shocks to prevent you from going back into debt and disrupting your repayment plan.

KEY POINT

An emergency fund (3-6 months’ expenses) is a critical defense against future debt. Build a starter fund ($1,000-$2,000) while tackling high-interest debt, then ramp up savings to fully protect your financial progress and prevent new debt cycles.

7. Real-World Developer Debt Scenarios

Let’s examine a couple of hypothetical scenarios to see how these strategies play out in a developer’s life in 2026. These examples highlight how tailored approaches can lead to significant progress.

Case Study 1: The New Grad with Credit Card & Student Loan Debt

Meet Alex: A junior full-stack developer earning $80,000 annually in a medium cost-of-living area. Alex graduated in 2025 with $45,000 in federal student loans (avg. 5.5% APR, $480 min payment, 10-year term). During their final year and job search, Alex accumulated $7,000 in credit card debt across two cards (Card X: $4,000 @ 26% APR, $100 min; Card Y: $3,000 @ 22% APR, $75 min). Alex has a $1,000 emergency fund already and wants to become debt-free quickly.

Alex’s Strategy: Debt Avalanche + Rigorous Budgeting

Alex’s priority is high-interest credit card debt. They use the Debt Avalanche method for maximum interest savings and commit to a tight budget.

Alex creates a strict budget, cutting discretionary spending significantly. By cooking more at home (saving $300/month), canceling unused streaming services ($50/month), and reducing impulse tech purchases ($250/month), Alex frees up an extra $600 per month. Here’s the plan for 2026:

- Pay minimums on Student Loan ($480) and Credit Card Y ($75).

- Direct all extra $600 + Credit Card X’s minimum ($100) = $700 towards Credit Card X (26% APR). This will pay off Card X in approximately 6 months.

- Once Card X is paid off (around October 2026), Alex takes the $700 (which was going to Card X) and adds it to Credit Card Y’s minimum ($75) = $775 towards Credit Card Y (22% APR). This will pay off Card Y in approximately 4 months.

- After Card Y is paid off (early 2027), Alex now has $775 + $480 (student loan min) = $1,255 to throw at the student loans, drastically accelerating their repayment.

Outcome: Alex eliminates $7,000 in credit card debt in about 10 months, saving hundreds in interest compared to making only minimum payments. This psychological boost and freed-up cash flow allow Alex to tackle the student loans much more aggressively. They also build strong financial habits early in their career.

Case Study 2: The Mid-Career Developer with Refinancing Opportunity

Meet Ben: A senior software engineer earning $140,000 annually in a high cost-of-living area. Ben has $30,000 remaining on private student loans (avg. 7.5% APR, $350 min payment, 8-year term) from a coding bootcamp and a small personal loan of $5,000 (12% APR, $150 min payment, 3-year term). Ben has an emergency fund of 6 months’ expenses and no credit card debt, giving him a stable financial position.

Ben’s Strategy: Refinance + Debt Snowball (for personal loan)

Ben has excellent credit and stable income, making refinancing a viable option for his private student loans, and then applies the Snowball method to his personal loan.

Ben researches private student loan refinancing options in early 2026. With his strong financial profile (credit score 780+), he qualifies for a new loan of $30,000 at 4.2% APR over a 7-year term, reducing his new monthly minimum payment to approximately $420. He decides to keep his payment at the old $350 level, effectively paying more than the new minimum to accelerate repayment, and has an extra $800 from his budget he wants to use for debt.

- Ben refinances his private student loan, lowering the APR from 7.5% to 4.2%. His new minimum payment is $420, but he continues to pay $350 toward this loan initially as part of his strategy.

- He then uses the Debt Snowball strategy, focusing his extra $800 + personal loan minimum ($150) = $950 on the $5,000 personal loan (12% APR). This will pay off the personal loan in approximately 5-6 months.

- Once the personal loan is paid off (around September 2026), he directs that $950 plus the original student loan payment amount ($350) towards his refinanced student loan, now paying $1,300 per month towards it.

Outcome: Ben saves thousands in interest on his student loans due to refinancing and quickly eliminates his personal loan. The freed-up cash flow allows him to aggressively pay down his lower-interest student loan, positioning him for significant wealth building and potentially buying a home sooner.

KEY POINT

Real-world scenarios demonstrate how combining budgeting, repayment methods (Avalanche for high interest, Snowball for quick wins), and advanced tactics like refinancing can dramatically accelerate debt freedom for developers, leading to substantial savings and faster financial goals.

8. Important Considerations & Caveats

Navigating debt management involves more than just numbers. There are broader financial implications and psychological aspects to consider as you work towards becoming debt-free in 2026. Being aware of these can help you make more informed decisions and stay motivated.

Impact on Your Credit Score

Paying down debt, especially high-interest credit card debt, generally has a positive impact on your credit score. Lowering your credit utilization ratio (the amount of credit you are using compared to your total available credit) is a significant factor in boosting your score, accounting for about 30% of your FICO score. Consistently making on-time payments, which is crucial for debt repayment, also positively impacts your payment history (35% of FICO score).

However, closing old accounts immediately after paying them off might slightly reduce your average age of accounts (15% of FICO score), which can have a minor, temporary negative effect. It is usually best to keep old, paid-off credit card accounts open if they do not have annual fees and you can resist the urge to use them. This helps maintain a longer credit history and higher available credit, keeping your utilization low.

Tax Implications of Debt

For some debts, there can be tax benefits or consequences that are important to understand:

- Student Loan Interest Deduction: In 2026, you can generally deduct up to $2,500 in student loan interest paid during the year. This deduction can reduce your taxable income, potentially saving you money on your federal income tax bill. Eligibility depends on your modified adjusted gross income (MAGI). For current rules and limits, always consult IRS Publication 970 or a qualified tax professional.

- Mortgage Interest Deduction: If you have a mortgage, the interest paid on it is usually deductible, subject to certain limits. This can be a significant tax break for homeowners.

- Debt Forgiveness: Be aware that if a creditor forgives a portion of your debt (e.g., in a settlement or bankruptcy), that forgiven amount might be considered taxable income by the IRS, unless you are insolvent (meaning your liabilities exceed your assets) at the time the debt is forgiven. This can lead to an unexpected tax bill.

The Psychological Toll of Debt

Debt is not just a financial burden; it can also take a significant psychological toll, leading to stress, anxiety, sleep disturbances, and even impacting relationships. Recognizing this aspect is important. To combat this, celebrate small victories, such as paying off your first credit card or reaching a specific balance reduction milestone. Stay consistent, and remember that every payment, no matter how small, is a step towards financial freedom. Do not hesitate to seek support from financial advisors for guidance or even mental health professionals if debt-related stress becomes overwhelming and starts affecting your daily life or work performance.

WARNING

Always consult with a qualified tax advisor or financial planner for personalized advice regarding tax implications and complex financial decisions, especially before making major changes like debt settlements or large refinances. Tax laws can be complex and change annually.

KEY POINT

Understand the impact of debt repayment on your credit score (credit utilization, payment history) and be aware of potential tax implications, such as the student loan interest deduction or debt forgiveness taxes, to optimize your financial strategy and avoid surprises.

Frequently Asked Questions (FAQ)

Q. Should I prioritize saving for retirement or paying off debt?

A. Generally, it is recommended to save enough in your 401(k) or similar retirement plan to get any employer match, as this is essentially free money (often a 50-100% return). After securing the match, prioritize high-interest debt (like credit cards with 15%+ APR). For lower-interest debt (like student loans under 6-7%), it can be a personal choice between investing more for retirement and accelerated debt repayment; consider your risk tolerance and projected investment returns.

Q. How long does it typically take to pay off credit card debt with a good income?

A. With a consistent extra payment strategy (like Avalanche or Snowball) and a developer’s salary, many can eliminate significant credit card debt ($5,000-$10,000) within 6 to 18 months, especially if they cut discretionary spending and maintain a strict budget. The exact timeline depends on the total balance, interest rates, and the amount of extra payments made each month.

Q. Is it ever a good idea to take out a personal loan to consolidate credit card debt?

A. Yes, if you can secure a personal loan with a significantly lower interest rate than your credit cards (e.g., 8-12% vs. 20%+), it can be a smart move. This converts multiple high-interest, revolving debts into a single, lower-interest installment loan with a fixed repayment schedule. However, ensure you do not then run up new balances on the old credit cards, as that would worsen your debt situation considerably.

Q. What are the risks of refinancing federal student loans?

A. Refinancing federal student loans with a private lender means losing valuable federal protections such as access to income-driven repayment plans (payments based on income), generous deferment and forbearance options (temporary payment pauses), and eligibility for federal loan forgiveness programs (e.g., Public Service Loan Forgiveness). While you might get a lower interest rate, these lost protections can be significant, especially if your financial situation changes unexpectedly.

Q. How often should I review my budget and debt repayment plan?

A. Regularly reviewing your budget and debt repayment plan is essential. Aim to assess your financial situation at least once a month to ensure you are on track and make adjustments as necessary based on changes in income, expenses, or financial goals.