SUMMARY

Automated Investing for Developers in 2026

Discover how automated investing and robo-advisors can simplify wealth building for busy developers, offering passive growth and long-term financial success.

Keywords: Automated Investing, Robo-Advisors, Passive Income

TABLE OF CONTENTS

1 Why Automated Investing? The Developer’s Advantage

2 Understanding Robo-Advisors: Your Digital Financial Partner

3 Top Robo-Advisors in 2026: A Kwonglish Deep Dive

4 Smart Strategies for Developers: Maximize Your Robo-Advisor

5 Real-World Scenarios: Developers & Robo-Advisors

6 Caveats, Considerations, and FAQs

OVERVIEW

Why Automated Investing? The Developer’s Advantage

Hey there, Kwonglish community! As developers, we’re always looking for efficient, automated solutions, whether it’s for deploying code, managing databases, or optimizing workflows. So why should our personal finances be any different? In 2026, the world of investing offers incredible tools to help busy tech professionals build wealth without diving deep into stock charts or economic forecasts: automated investing and robo-advisors.

We know your time is precious. You’re probably juggling complex projects, learning new frameworks, and maybe even debugging late into the night. The last thing you want is another complex system to manage, especially when it comes to your hard-earned money. That’s where automated investing shines. It’s designed to take the guesswork and the heavy lifting out of growing your wealth, allowing you to focus on what you do best: building amazing software.

“Automated investing isn’t just a convenience; it’s a strategic advantage for developers, transforming complex financial decisions into streamlined, code-like processes.”

— Kwonglish Insight

This guide will walk you through everything you need to know about setting up a robust, passive investment strategy for 2026 and beyond. We’ll explore what robo-advisors are, compare the top platforms, discuss smart strategies tailored for a developer’s lifestyle, and address common questions and concerns. Our goal is to empower you to make informed decisions that pave the way for long-term financial security and freedom.

KEY POINT

Automated investing leverages technology to manage your investments, providing a hands-off approach that’s ideal for time-constrained professionals like developers. It focuses on long-term growth through diversified portfolios and algorithmic rebalancing.

CORE GUIDE

Understanding Robo-Advisors: Your Digital Financial Partner

At its core, a robo-advisor is a digital platform that provides automated, algorithm-driven financial planning services with little to no human supervision. It’s like having a personal financial advisor, but one that runs on code, making it more accessible, affordable, and often, more objective.

How Robo-Advisors Work

When you sign up for a robo-advisor, you’ll typically complete a questionnaire that assesses your financial goals, risk tolerance, and time horizon. Based on your answers, the algorithm constructs a diversified portfolio of low-cost exchange-traded funds (ETFs) and mutual funds. These portfolios are usually diversified across various asset classes, such as:

☑ U.S. Stocks: For growth potential.

☑ International Stocks: For global diversification.

☑ Bonds: For stability and income.

☑ Real Estate (REITs): For additional diversification and income potential.

Once your portfolio is set, the robo-advisor handles the ongoing management, including:

✓ Automatic Rebalancing: Keeping your asset allocation consistent with your risk profile.

✓ Dividend Reinvestment: Automatically reinvesting any dividends earned back into your portfolio.

✓ Tax-Loss Harvesting: Selling investments at a loss to offset capital gains and potentially ordinary income, a feature often found in higher-tier services.

✓ Goal Tracking: Helping you visualize progress towards specific financial goals like retirement or a down payment.

KEY POINT

Robo-advisors are particularly effective for long-term investors who prioritize low fees, diversification, and a hands-off approach. They are not designed for active trading or complex, bespoke financial planning needs.

Benefits for Developers

For developers, the advantages are clear:

Developer-Centric Benefits

Time Efficiency — Set it and forget it. No need to monitor markets daily or research individual stocks.

Low Costs — Advisory fees typically range from 0.25% to 0.50% of assets under management (AUM), significantly lower than traditional financial advisors (who often charge 1% or more).

Automation — Rebalancing, dividend reinvestment, and tax-loss harvesting are handled automatically, just like a well-crafted CI/CD pipeline.

Diversification — Built-in diversification across various asset classes minimizes risk, a critical component of sound long-term investing.

Objectivity — Algorithms don’t get emotional during market fluctuations, helping you stick to your long-term plan.

Pros

✓ Cost-effective wealth management

✓ Hands-off investment approach

✓ Diversified portfolios for risk mitigation

✓ Automated tax-efficiency features

✓ Accessible with low minimums

Cons

✗ Less personalized advice than human advisors

✗ Limited customization for specific stock/fund picks

✗ May not be ideal for very complex financial situations

✗ Some platforms have cash allocations that might underperform in bull markets

PLATFORM DEEP DIVE

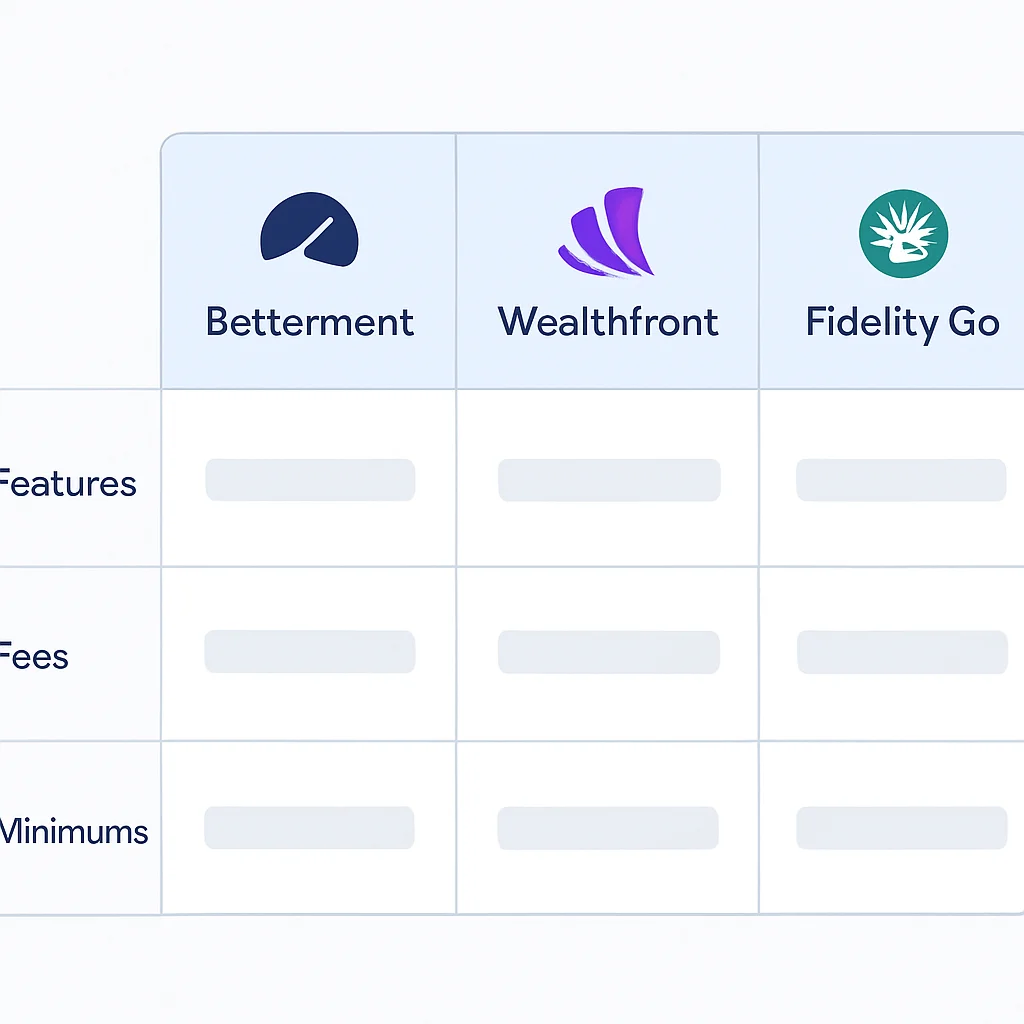

Top Robo-Advisors in 2026: A Kwonglish Deep Dive

The robo-advisor landscape continues to evolve, with platforms constantly adding new features and refining their algorithms. Here’s a look at some of the top contenders in 2026, keeping in mind the needs of a developer.

1. Betterment: The Pioneer with Robust Features

Betterment Highlights

Minimum Investment: $0 (for Digital Plan), $100,000 (for Premium Plan)

Advisory Fees: 0.25% AUM (Digital), 0.40% AUM (Premium)

Key Features: Goal-based planning, advanced tax-loss harvesting, flexible portfolios, access to human advisors (Premium), cash management.

Betterment remains a strong choice for developers due to its comprehensive approach to financial planning. Its automated tax-loss harvesting can be a significant advantage, especially for those with sizable taxable brokerage accounts. The platform’s user interface is intuitive, making it easy to set up goals like retirement, a down payment, or simply general investing. For those who eventually want a human touch, the Premium plan offers unlimited calls with certified financial planners.

2. Wealthfront: Tech-Forward for Growth-Oriented Investors

Wealthfront Highlights

Minimum Investment: $500

Advisory Fees: 0.25% AUM

Key Features: Advanced tax-loss harvesting (daily), Smart Beta for larger accounts, Path (financial planning tool), crypto trusts, cash account with competitive APY.

Wealthfront appeals to developers with its emphasis on technology and advanced features. Their “Path” tool offers sophisticated financial planning, allowing you to model various life events and their impact on your finances. For higher balances ($100,000+), their Smart Beta strategy aims to deliver higher returns by weighting stocks based on factors like value and momentum, which might resonate with developers interested in quantitative strategies. Their daily tax-loss harvesting is also a standout feature.

3. Fidelity Go: Seamless Integration for Fidelity Users

Fidelity Go Highlights

Minimum Investment: $0 to open, $0 advisory fee for balances under $25,000, $500 to start investing

Advisory Fees: 0% for balances under $25,000; 0.35% AUM for balances over $25,000

Key Features: No advisory fees for smaller balances, uses Fidelity Flex® mutual funds (no expense ratios), seamless integration with existing Fidelity accounts.

If you already have a 401(k) or other accounts with Fidelity, Fidelity Go offers a convenient and integrated solution. The biggest draw is the $0 advisory fee for balances under $25,000, making it incredibly accessible for new investors or those just starting their automated journey. While it doesn’t offer advanced features like tax-loss harvesting, its simplicity and fee structure for smaller accounts make it a compelling option. The portfolios utilize Fidelity’s own low-cost funds, which have no additional expense ratios.

KEY POINT

When choosing a robo-advisor, consider its fee structure, minimum investment, tax-efficiency features (like tax-loss harvesting), and whether it offers access to human advisors if that’s important to you. Each platform has its strengths tailored to different investor profiles.

STRATEGY GUIDE

Smart Strategies for Developers: Maximize Your Robo-Advisor

You’ve picked your platform, now let’s talk strategy. As developers, we appreciate robust systems and predictable outcomes. Applying a few core principles can significantly enhance your automated investing journey.

1. Embrace Dollar-Cost Averaging (DCA)

This is perhaps the most fundamental and effective strategy for long-term investors, especially with automated platforms. DCA involves investing a fixed amount of money at regular intervals (e.g., $500 every month), regardless of market fluctuations. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more. Over time, this averages out your purchase price and reduces the risk of trying to “time the market.”

1

Set Up Automatic Transfers

Configure your robo-advisor to automatically pull a set amount from your bank account bi-weekly or monthly. This ensures consistency and leverages the power of DCA.

2. Understand and Set Your Risk Tolerance

Every robo-advisor starts with a questionnaire to gauge your risk tolerance. Be honest! If you panic and sell during a market downturn, a more aggressive portfolio will hurt you more. A portfolio that aligns with your comfort level will help you stay invested through volatility.

WARNING

Overstating your risk tolerance to achieve higher potential returns can lead to emotional decisions during market corrections. Stick to a risk level that allows you to sleep soundly at night.

3. Maximize Tax Efficiency

Developers often have higher incomes, making tax efficiency a crucial component of their investment strategy.

☑ Contribute to Tax-Advantaged Accounts First: Max out your 401(k), IRA (Traditional or Roth), and HSA before contributing to a taxable brokerage account. These accounts offer significant tax benefits.

☑ Utilize Tax-Loss Harvesting: As mentioned, many robo-advisors offer automated tax-loss harvesting. This feature sells investments at a loss to offset capital gains and, to a limited extent ($3,000 per year), ordinary income. Over years, this can save you thousands in taxes.

☑ Asset Location: Some advanced robo-advisors or human advisors can help with “asset location,” placing tax-inefficient assets (like bonds, which generate ordinary income) in tax-advantaged accounts and growth-oriented assets (like stocks, which generate capital gains) in taxable accounts. While this might be a bit too granular for basic robo-advisors, it’s good to be aware of for future planning.

KEY POINT

For developers, the “set it and forget it” nature of robo-advisors complements a busy schedule. Focus on consistent contributions (DCA), align with your true risk tolerance, and leverage tax-efficient features to maximize long-term growth.

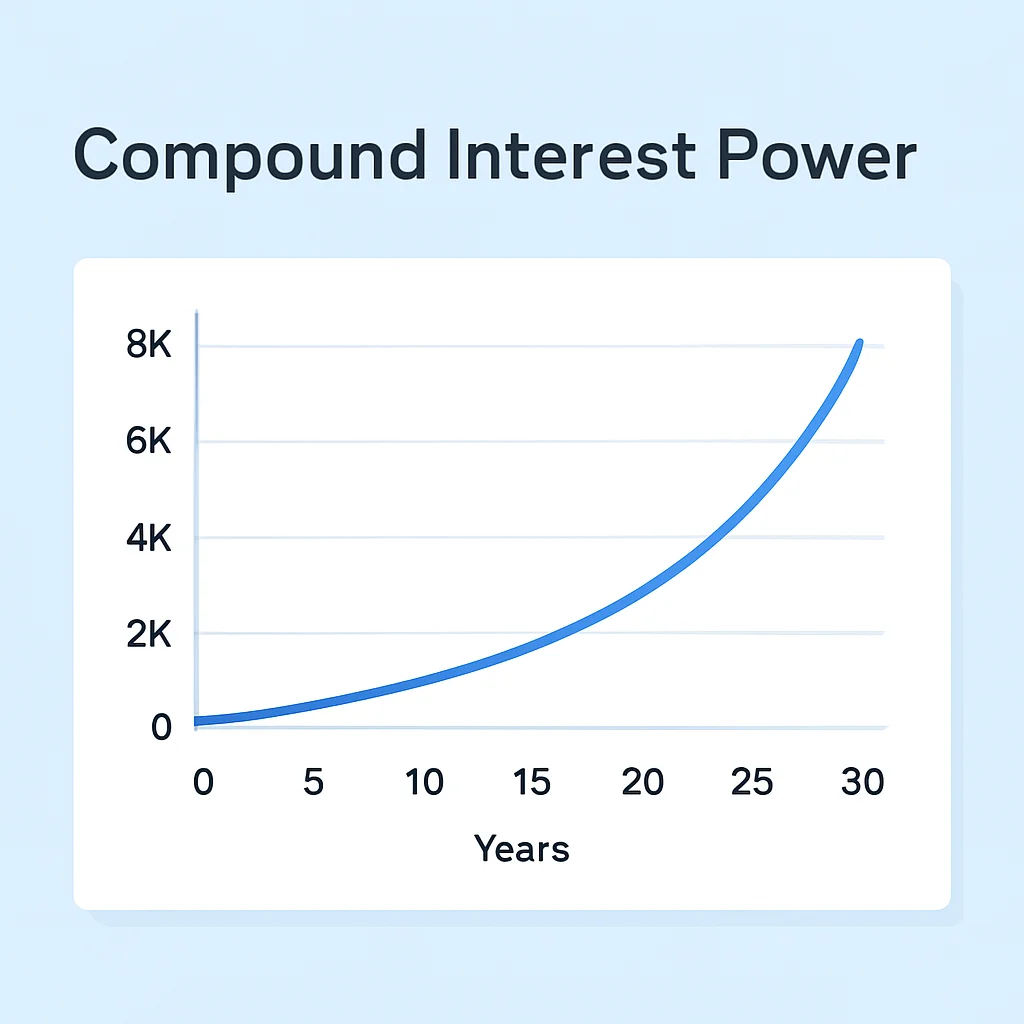

Example: Calculating Compound Interest (A Developer’s Favorite)

Let’s put on our developer hats for a moment. Understanding the power of compound interest is crucial. Here’s a simple Python script to illustrate how your investments can grow over time with consistent contributions. This isn’t something your robo-advisor does for you directly, but it’s a fundamental concept that underlies its effectiveness.

CODE EXPLANATION

This Python script calculates the future value of an investment with regular monthly contributions, demonstrating the power of compound interest. You can adjust the initial investment, monthly contribution, annual return rate, and number of years to see different scenarios.

def calculate_compound_interest(initial_investment, monthly_contribution, annual_return_rate, years):

"""

Calculates the future value of an investment with monthly contributions.

Args:

initial_investment (float): The starting amount.

monthly_contribution (float): Amount contributed each month.

annual_return_rate (float): Annual expected return rate (e.g., 0.07 for 7%).

years (int): Number of years to invest.

Returns:

float: The total future value of the investment.

"""

monthly_return_rate = annual_return_rate / 12

total_months = years * 12

future_value = initial_investment

for _ in range(total_months):

future_value = (future_value + monthly_contribution) * (1 + monthly_return_rate)

return future_value

# --- Configuration for a typical developer ---

initial_investment_kwonglish = 5000 # Starting with some savings

monthly_contribution_kwonglish = 800 # Consistent monthly investment

annual_return_rate_kwonglish = 0.07 # Assumed average annual return (7%)

years_kwonglish = 20 # Investing for 20 years

# Calculate and print the results

final_amount = calculate_compound_interest(

initial_investment_kwonglish,

monthly_contribution_kwonglish,

annual_return_rate_kwonglish,

years_kwonglish

)

print(f"Initial Investment: ${initial_investment_kwonglish:,.2f}")

print(f"Monthly Contribution: ${monthly_contribution_kwonglish:,.2f}")

print(f"Annual Return Rate: {annual_return_rate_kwonglish*100:.0f}%")

print(f"Investment Period: {years_kwonglish} years")

print(f"Estimated Future Value: ${final_amount:,.2f} in 20{26 + years_kwonglish}")

# Example for a shorter period

print("\n--- Shorter Period Example (10 years) ---")

years_short = 10

final_amount_short = calculate_compound_interest(

initial_investment_kwonglish,

monthly_contribution_kwonglish,

annual_return_rate_kwonglish,

years_short

)

print(f"Estimated Future Value (10 years): ${final_amount_short:,.2f} in 20{26 + years_short}")

Running this script with the provided parameters (e.g., $5,000 initial, $800 monthly, 7% annual return for 20 years), you’d see an estimated future value of approximately $408,000. This dramatically illustrates how consistent, automated investing, even with modest contributions, can lead to substantial wealth over time. Your robo-advisor does the heavy lifting of managing the underlying investments to achieve that return.

REAL-WORLD CASES

Real-World Scenarios: Developers & Robo-Advisors

Let’s look at how different developers might leverage robo-advisors to achieve their financial goals in 2026.

Case 1: The Junior Developer — Starting Small, Thinking Big

Scenario: Alex, 24, Junior Front-End Developer

Alex has just landed his first full-time dev job. He has some student loan debt but also wants to start saving for a house down payment in about 7-10 years. He has limited savings and wants a hands-off approach.

Robo-Advisor Solution: Alex chooses Fidelity Go. With a $0 minimum to open and no advisory fee for balances under $25,000, it’s perfect for his current budget. He sets up an automatic monthly transfer of $250 from his checking account and selects a moderately conservative portfolio given his medium-term goal. He loves that he doesn’t have to think about it, allowing him to focus on mastering React and paying down his loans.

KEY POINT

Robo-advisors with low or no minimums and tiered fee structures (like Fidelity Go) are excellent entry points for junior developers or those with limited initial capital.

Case 2: The Mid-Level Engineer — Optimizing Growth, Minimizing Taxes

Scenario: Brenda, 32, Senior Software Engineer

Brenda has a solid income, maxes out her 401(k) and IRA, and now has significant savings in a taxable brokerage account. She wants to optimize her investment growth and minimize her tax burden, ideally with minimal manual intervention.

Robo-Advisor Solution: Brenda chooses Wealthfront. Its advanced tax-loss harvesting and Smart Beta option for larger accounts align perfectly with her goals. She transfers her taxable brokerage account to Wealthfront, where the algorithm continuously looks for opportunities to harvest losses, offsetting capital gains from her company stock options and other investments. She maintains a growth-oriented portfolio, confident that Wealthfront is working to enhance her after-tax returns.

Case 3: The Senior Architect — Comprehensive Planning for Retirement

Scenario: Chris, 45, Principal Architect

Chris has accumulated substantial wealth across various accounts (401k, IRA, taxable, HSA) and is planning for early retirement in 10-15 years. He wants a comprehensive overview of his finances and reassurance that he’s on track, with the option to consult a human advisor occasionally.

Robo-Advisor Solution: Chris opts for Betterment’s Premium Plan. While his core investments are managed automatically with tax-loss harvesting, the Premium plan provides unlimited access to certified financial planners. This allows him to get personalized advice on complex topics like estate planning, withdrawal strategies, or integrating his stock options into his overall financial plan, all while the automated system handles the day-to-day investing. Betterment’s goal-setting tools also help him visualize his path to early retirement.

“The beauty of modern robo-advisors is their flexibility to adapt to different financial stages, from a junior developer’s first dollar to a principal architect’s retirement planning.”

— Kwonglish Perspective

CAVEATS & FAQ

Caveats, Considerations, and FAQs

While automated investing offers significant advantages, it’s important to be aware of its limitations and when a human touch might still be necessary.

When Robo-Advisors Might Not Be Enough

Robo-advisors excel at portfolio management, but they have limitations:

✗ Complex Financial Planning: If you have intricate tax situations, own a business, manage significant real estate, have special needs dependents, or require complex estate planning, a dedicated human financial advisor is often a better choice. They can offer holistic advice that goes beyond investment management.

✗ Behavioral Coaching: While algorithms are objective, humans sometimes need a coach to prevent emotional decisions during market downturns. Some robo-advisors offer access to human advisors for this reason, but it’s not their primary function.

✗ Highly Customized Portfolios: If you want to invest in specific individual stocks, alternative assets (beyond what’s offered), or have very niche investment preferences, a robo-advisor’s diversified ETF portfolios might feel too generic.

WARNING

Always understand the fee structure, including both the advisory fee and the underlying expense ratios of the ETFs. Even small fees can significantly erode returns over decades.

Frequently Asked Questions (FAQ)

Q. Are robo-advisors safe?

A. Yes, reputable robo-advisors are typically regulated by the SEC and offer SIPC insurance, which protects your investments up to $500,000 in case the brokerage fails. They invest in diversified portfolios, which inherently reduces risk compared to individual stock picking.

Q. How much control do I have over my investments with a robo-advisor?

A. You control your risk tolerance and financial goals, which dictates your portfolio’s asset allocation. While you don’t pick individual stocks or ETFs, most platforms allow you to adjust your risk profile or even select specific themed portfolios (e.g., socially responsible investing).

Q. What happens during a market downturn?

A. Robo-advisors are designed for long-term investing. During downturns, they will continue to rebalance your portfolio and, if enabled, perform tax-loss harvesting. This systematic approach helps you buy low and maintain your target asset allocation, preventing emotional selling that often harms investor returns.

Q. Can I link my external accounts to a robo-advisor?

A. Many robo-advisors, especially those with more comprehensive financial planning tools like Betterment or Wealthfront, allow you to link external accounts (e.g., 401k, bank accounts, credit cards) for a holistic view of your finances. This helps their algorithms provide more accurate advice and goal tracking.

Q. Are robo-advisors only for beginners?

A. Absolutely not. While great for beginners due to their simplicity and low minimums, many experienced investors and high-net-worth individuals use robo-advisors for efficient management of portions of their portfolios, especially for taxable accounts where features like tax-loss harvesting provide significant value.

WRAP-UP

Simplifying Wealth for the Tech-Savvy

As developers, we build systems that automate complex tasks and streamline processes. It’s only natural that we apply the same principles to our personal finance. Automated investing through robo-advisors offers a powerful, low-cost, and efficient way to grow your wealth in 2026 and for decades to come.

“The best investment you can make is in your long-term financial well-being, and for busy developers, automated investing is a crucial tool in that arsenal.”

— Kwonglish Philosophy

By understanding how these platforms work, choosing the right one for your needs, and adopting smart strategies like dollar-cost averaging and maximizing tax efficiency, you can build a robust financial future. So, go ahead, set up your automated investments, and then get back to writing that elegant code — knowing your money is working hard for you in the background.

REFERENCES

Betterment Official Site

Wealthfront Official Site

Fidelity Go Official Site

Investopedia: Robo-Advisor

Ready to Automate Your Wealth?

We hope this guide has demystified automated investing and shown you how robo-advisors can be a powerful tool in your financial journey. Start building your passive income stream today!

Got questions or favorite robo-advisor tips? Drop a comment below! We’d love to hear from you.